The Hidden Enemy: How Simple Mistakes on Your Credit Report Quietly Drain Your Wallet

Written by: Kamal Uddin, Financial Writer & Credit Coach

Reviewed and Fact-Checked by: David Miller, Certified Financial Planner (CFP)

Last Updated: July 2026 | Reviewed for FCRA Compliance

About the Author & Fact-Checker

Kamal Uddin is an experienced credit coach and consumer finance writer. Over the past decade, he has helped hundreds of everyday consumers navigate the complexities of the Fair Credit Reporting Act (FCRA) to correct errors, rebuild their credit scores, and regain control of their financial futures.

David Miller, CFP®, is a certified financial planner and consumer rights advocate. He meticulously reviews and fact-checks this content to ensure that all financial strategies, legal references, and credit repair guidelines align with current regulatory standards and best practices.

🌐 Important Notice for International Readers:

This comprehensive guide is specifically tailored for consumers in the United States. The credit reporting systems, dispute mechanisms, and legal protections mentioned—such as the Fair Credit Reporting Act (FCRA) and the Consumer Financial Protection Bureau (CFPB)—operate strictly within U.S. federal jurisdiction and do not apply directly to credit systems in other countries.

You apply for a car loan, and the dealer looks at you with pity. Your heart sinks because you know your score is low, but you have no idea why you keep falling behind. You pay your bills on time, you work long hours, and you try your best to stay afloat.

Yet, you are stuck paying huge interest rates, or worse, you get rejected outright. The worst part is that you might be paying for mistakes you never made. A single typo by a bank clerk can label you as a high-risk borrower.

This is the quiet reality for millions of hardworking people. They are locked out of their dreams because of simple paperwork errors. It is a frustrating barrier that keeps you from moving forward in life.

Why Finding the Right Credit Help Feels Impossible

- Many online forums suggest paying expensive credit repair agencies that often do nothing but send a template letter you could write yourself.

- Some popular websites tell you to close old accounts, which actually lowers your score and makes your financial situation worse.

- Dozens of blogs push new credit cards that promise to build credit but end up charging high annual fees and interest.

- Many sources fail to explain the difference between a real dispute and just complaining, leaving you confused about the exact rules.

- You often find guides that tell you to dispute everything at once, which makes the credit bureaus flag your request as fake.

- Most advice assumes you have thousands of dollars to pay off debts, ignoring the fact that simple errors might be the main issue.

The Mental and Emotional Weight of a Bad Credit Score

- You feel a constant sense of shame when renting an apartment, wondering if the landlord will reject your application.

- It causes silent tension at home because you cannot qualify for a mortgage to build a stable future for your family.

- Your sleep suffers as you stay awake calculating how much money you are losing to high-interest rates.

- It chips away at your self-confidence, making you feel like a financial failure even when you are incredibly responsible.

- You start avoiding your mailbox and your phone calls, fearing another collection agency notice that does not even belong to you.

- This constant stress can drain your energy, making it hard to focus on your job or enjoy your daily life.

Understanding the Real Cost of System Mistakes

Let us be honest about how the credit system works. The credit bureaus do not know you as a person. They only see you as a series of numbers and data points on a screen.

These bureaus handle billions of pieces of data every single month. With that much data moving around, mistakes are bound to happen. In fact, studies show that one in four credit reports contain errors that can ruin a score.

Think of it like buying groceries at your local store. If the cashier accidentally scans an item twice, you do not just pay the extra bill and walk away. You speak up, point out the error, and ask for a refund.

Your credit score deserves that same level of care. When there is a mistake on your report, it acts like a leak in a water bucket. No matter how much water you pour in, the bucket never fills up.

You can pay every single bill on time, but that one error will keep dragging your score down. Fixing these errors is not about gaming the system. It is about making sure the system tells the truth about your financial habits.

Your Simple Action Plan: How to Clean Up Your Credit History

Now that we understand the problem, let us look at the solution. You do not need to pay a lawyer hundreds of dollars to fix this. You can do this yourself with a little time and a clear plan.

We will focus on the first three steps to clean up your credit file. These steps are designed to be easy to follow and highly effective. Let us get started on reclaiming your financial reputation.

Step 1: Pull Your Free Credit Reports and Find the Hidden Errors

The first step is to see exactly what the credit bureaus are saying about you. You cannot fix a problem if you do not know where it is. You need to get your official reports from the three major bureaus.

<div style="overflow-x: auto; margin: 20px 0;">

<table style="width:100%; border-collapse: collapse; font-family: sans-serif; text-align: center; border: 1px solid #ddd;">

<thead>

<tr style="background-color: #f2f2f2;">

<th colspan="3" style="padding: 12px; border: 1px solid #ddd; font-weight: bold;">THE THREE MAJOR CREDIT BUREAUS</th>

</tr>

</thead>

<tbody>

<tr>

<td style="padding: 15px; border: 1px solid #ddd; font-weight: bold; width: 33.33%;">Equifax</td>

<td style="padding: 15px; border: 1px solid #ddd; font-weight: bold; width: 33.33%;">Experian</td>

<td style="padding: 15px; border: 1px solid #ddd; font-weight: bold; width: 33.33%;">TransUnion</td>

</tr>

</tbody>

</table>

</div>

You can get these reports for free by using the official website, AnnualCreditReport.com. Do not use websites that ask for your credit card number or offer trial subscriptions. The law guarantees you access to these reports without any cost.

Once you have your reports, print them out or save them as PDF files. Grab a colored highlighter or use a digital tool to mark anything that looks wrong. You want to look at every single line with a critical eye.

Common Personal Information Errors to Look For

Start at the very top of your report where your personal details are listed. Check your name, address, and social security number.

- Misspelled Names: A simple typo in your name can mix your file with someone else's file.

- Old Addresses: If an address you never lived at is listed, it could be a sign of identity theft.

- Wrong Employers: Incorrect work history can make you look unstable to future lenders.

Account Status Errors That Hurt Your Score

Next, move down to the active and closed accounts section. This is where the most damaging mistakes usually hide.

- Closed Accounts Listed as Open: If you closed an account, it should say "closed by consumer" instead of active.

- Incorrect Payment History: Look closely at the late payment calendar for each account. If you paid on time, but it shows a thirty-day late status, highlight it immediately.

- Wrong Balance Amounts: Compare the balances on the report with your actual bank statements from that month.

- Duplicate Accounts: Sometimes, a single debt is listed multiple times, especially if it was sold to a collection agency.

The Danger of Mixed Files

A mixed file happens when the credit bureau combines your information with another person who has a similar name. For example, if your name is John Smith, you might see credit cards belonging to a different John Smith on your report.

This is highly common and can destroy your score overnight if the other person has bad habits. If you see accounts you never opened, this is a major red flag. Do not panic, as we will show you exactly how to dispute these.

What to Do If You Are a Victim of Identity Theft

If you see unfamiliar accounts and suspect your identity has been stolen, simply writing a standard dispute letter might not be enough. In this severe case, you should immediately file an official Identity Theft Report. You can do this online at IdentityTheft.gov.

Once you file the report, obtain a copy of the FTC Identity Theft Report and file a report with your local police department. Sending copies of these official law enforcement documents to the credit bureaus legally obligates them to block the fraudulent information from appearing on your report within four business days, bypassing the standard 30-day investigation timeline.

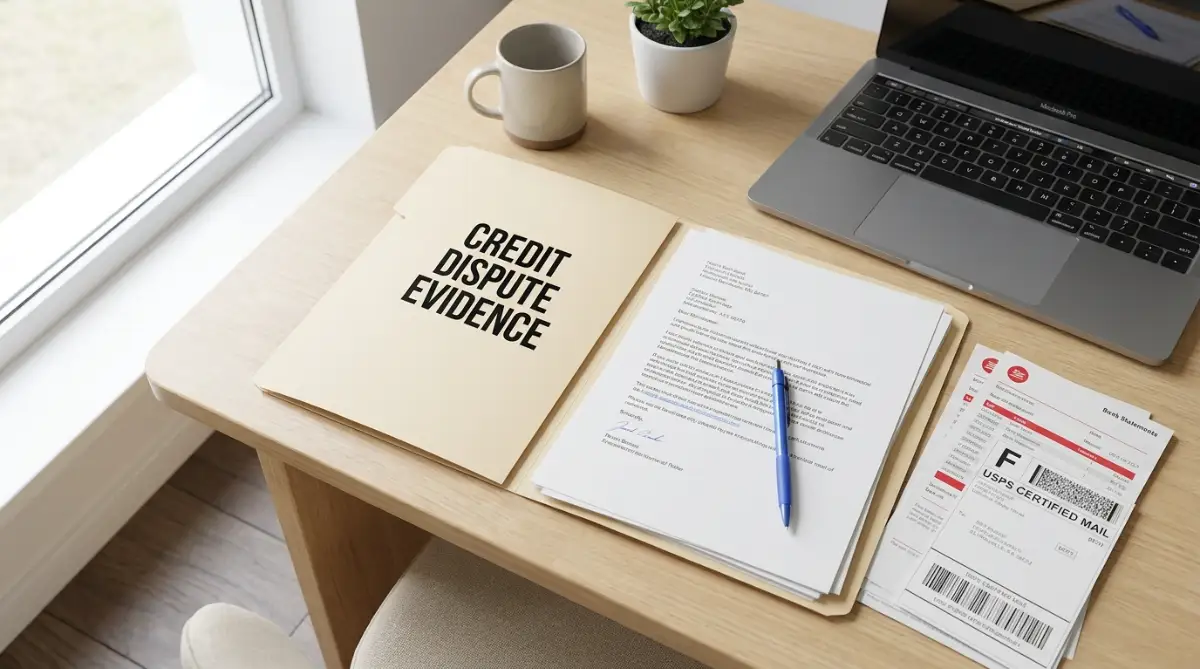

Step 2: Gather Your Proof Like a Professional Investigator

Once you have highlighted the errors, you need to collect your evidence. The credit bureaus will not take your word for it. They need physical proof to make a change.

If you claim a bill was paid on time, you must prove it. If you claim an account does not belong to you, you must show why. Gathering this proof is the most important part of the entire process.

The Document Checklist for Your Dispute

Create a folder on your computer or a physical folder on your desk. Collect the following documents based on the errors you found:

- Bank Statements: Show the exact date a payment cleared your account to prove you were not late.

- Canceled Checks: These serve as undeniable proof of payment to a creditor.

- ID Documents: A copy of your driver's license, utility bill, and social security card to prove your identity.

- Correspondence: Any emails or letters from the creditor showing they agreed to update your account status.

Let us look at a real-life scenario to see how this works. Imagine you paid off a credit card balance in full. However, your report still shows a five-hundred-dollar balance.

To prove this error, you would locate the specific bank statement showing the final payment leaving your account. You would also print the final statement from the credit card company showing a zero balance.

[Your Bank Statement] + [Credit Card Statement with $0] = Your Bulletproof Evidence

Having these two documents makes it nearly impossible for the credit bureau to reject your claim. They must update the information when faced with clear facts.

Organizing Your Evidence for Maximum Clarity

Do not just throw a pile of papers at the credit bureaus. They review thousands of disputes every day, and they prefer clear files.

Label each document clearly. For example, name a file "Bank_Statement_May_Payment.pdf" instead of a random string of numbers.

Write a brief note explaining what each document proves. This extra step helps the credit bureau employee understand your case in seconds. It reduces the chance of them rejecting your dispute due to confusion.

Case Study: How a $12,000 Typo Was Resolved

To understand the power of gathered proof, let's look at a case from my credit coaching files. In late 2025, a client named Sarah was repeatedly rejected for a modest auto loan. Her report showed an active $12,000 collection account from a bank she had never done business with.

Upon closer inspection, we realized this was a mixed-file error—the debt belonged to another consumer with a very similar name and birth year.

Instead of just complaining, Sarah gathered her identity verification documents (utility bills, Social Security card copy, and passport) and sent them alongside a formal dispute letter. When confronted with clear physical proof that she was not the debtor, the credit bureau deleted the incorrect $12,000 collection within two weeks. Sarah's credit score recovered by 115 points, allowing her to secure her car loan at a fair interest rate. Proper documentation is your best shield.

Step 3: Write and Send a High-Impact Dispute Letter

Now you are ready to write your dispute letter. You must write a separate letter to each credit bureau that has the error on your report.

Do not use pre-written online templates that sound like a lawyer wrote them. The credit bureaus use automated systems to scan for these generic letters. If they spot a template, they might label your dispute as spam.

Instead, write in your own words. Keep your tone polite, direct, and factual. You want to explain the error, explain why it is wrong, and state what action you want them to take.

The Simple Dispute Letter Structure

Your letter should follow a basic structure that is easy to read.

- Your Contact Info: Put your full name, address, and phone number at the very top.

- The Date: Always include the current date for record-keeping.

- The Bureau Address: Address it to the specific dispute department of Equifax, Experian, or TransUnion.

- The Main Body: Clearly state which account has the error and use the account number from your report.

- The Request: Ask them to correct or delete the item based on your evidence.

- The List of Attachments: Mention the specific documents you are enclosing with the letter.

A Ready-to-Use Dispute Letter Template

To help you get started, here is a simple, factual template you can copy and customize. Avoid copying it word-for-word; rewrite parts of it in your own handwriting or style so it does not look like an automated form letter.

[Your Full Name] [Your Current Mailing Address] [Your Phone Number] [Your Date of Birth] [Your Social Security Number] Date: [Current Date] [Name of Credit Bureau: Equifax / Experian / TransUnion] [Credit Bureau Dispute Department Address] Subject: Dispute of Inaccurate Information on My Credit Report To Whom It May Concern, I am writing to formally dispute several inaccurate items appearing on my credit report. I have recently reviewed my report and identified information that is incorrect and damaging to my financial standing. Below are the specific errors I wish to dispute: 1. Creditor Name: [Name of Bank/Creditor, e.g., Chase Bank] Account Number: [Account Number from your report] Type of Error: [Describe the error, e.g., "This account is listed as active, but it was closed by consumer in December 2024."] Supporting Evidence: [Name of attached document, e.g., "Attached is a letter from Chase Bank confirming the account closure."] 2. Creditor Name: [Name of Bank/Creditor, e.g., Capital One] Account Number: [Account Number from your report] Type of Error: [e.g., "The payment history shows a 30-day late payment for May 2025, but this payment was made on time."] Supporting Evidence: [e.g., "Attached is my bank statement from May 2025 showing the payment cleared on time."] Under the Fair Credit Reporting Act (FCRA), I request that you investigate these items and correct or delete them from my credit file as they cannot be verified. Please find enclosed a copy of my driver's license, a recent utility bill to verify my identity, and the supporting evidence documents listed above. I look forward to receiving your response and the results of your investigation within the legally mandated timeframe. Sincerely, [Your Signature] [Your Printed Name] Enclosures: - Copy of Driver’s License - Copy of Utility Bill - [List of evidence documents, e.g., Bank Statement, Closure Letter]

📥 Need a printable version?

<!-- Download Button -->

<div style="text-align: center; margin: 30px 0;">

<p style="font-size: 16px; font-weight: bold; margin-bottom: 10px;">📥 Need a printable version to customize at home?</p>

<a href="https://yourwebsite.com/downloads/free-credit-dispute-letter-template.docx" style="background-color: #28a745; color: white; padding: 12px 25px; text-decoration: none; border-radius: 5px; font-weight: bold; display: inline-block; box-shadow: 0 4px 6px rgba(0,0,0,0.1); transition: background-color 0.3s;" onmouseover="this.style.backgroundColor='#218838'" onmouseout="this.style.backgroundColor='#28a745'">

Download Free Dispute Letter Template (.docx)

</a>

</div>

📍 Official Mailing Addresses for the Major Credit Bureaus

To submit your physical dispute letter, you must send a separate copy to each of the credit bureaus reporting the error. Use the official addresses listed below:

- Equifax Information Services LLC

- P.O. Box 105069

- Atlanta, GA 30348-5069

- Experian

- P.O. Box 9701

- Allen, TX 75013

- TransUnion Consumer Solutions

- P.O. Box 2000

- Chester, PA 19016

(Note: We highly recommend checking each bureau's official website prior to mailing, as designated PO boxes for disputes can occasionally be updated by the credit bureaus.)

Alternative Route: Disputing Directly with the Creditor (The Direct Dispute Rule)

While sending disputes to the credit bureaus is the most common path, the Fair Credit Reporting Act (FCRA) also grants you the right to dispute inaccurate information directly with the "furnisher" (the bank, credit card issuer, or collection agency that reported the data).

Under the FCRA's Furnisher Rule, if you send a direct dispute letter containing your evidence to the creditor's designated address for disputes, they are legally obligated to investigate the error and report their findings back to you within 30 days. This is highly effective because it forces the bank to check their internal systems immediately, rather than waiting for a credit bureau to contact them.

Why Certified Mail is Your Secret Weapon

Never send your dispute letter by regular mail. You must send it via Certified Mail with a Return Receipt Requested.

This service costs a few dollars, but it is worth every penny. It gives you official proof that the credit bureau received your letter. It also shows them the exact date it arrived.

This date is highly important because of a consumer protection law called the Fair Credit Reporting Act (FCRA). Under this law, credit bureaus must investigate your dispute within 30 days of receiving it.

<div style="overflow-x: auto; margin: 20px 0;">

<table style="width:100%; border-collapse: collapse; font-family: sans-serif; border: 1px solid #ddd;">

<thead>

<tr style="background-color: #0056b3; color: white;">

<th colspan="2" style="padding: 12px; text-align: center; border: 1px solid #ddd;">THE 30-DAY DISPUTE TIMELINE</th>

</tr>

</thead>

<tbody>

<tr>

<td style="padding: 10px; border: 1px solid #ddd; font-weight: bold; width: 30%;">Day 1</td>

<td style="padding: 10px; border: 1px solid #ddd;">Bureau receives your Certified Mail and the clock starts.</td>

</tr>

<tr style="background-color: #f9f9f9;">

<td style="padding: 10px; border: 1px solid #ddd; font-weight: bold;">Day 2 to 29</td>

<td style="padding: 10px; border: 1px solid #ddd;">Bureau reviews your dispute, processes evidence, and contacts the creditor.</td>

</tr>

<tr>

<td style="padding: 10px; border: 1px solid #ddd; font-weight: bold;">Day 30</td>

<td style="padding: 10px; border: 1px solid #ddd;">Bureau must complete their official investigation and send you the results.</td>

</tr>

<tr style="background-color: #f9f9f9;">

<td style="padding: 10px; border: 1px solid #ddd; font-weight: bold; color: #d9534f;">Day 31+</td>

<td style="padding: 10px; border: 1px solid #ddd; font-weight: bold; color: #d9534f;">Any unverified or unanswered disputed items must be permanently deleted.</td>

</tr>

</tbody>

</table>

</div>

Important Note on the Timeline: While the standard investigation window is 30 days, please be aware that under the Fair Credit Reporting Act (FCRA), credit bureaus are allowed up to 45 days to investigate if you submitted your dispute after obtaining your credit report through the official AnnualCreditReport.com website, or if you send additional evidence while an investigation is already in progress. Plan your follow-up timeline accordingly.

If they do not finish their investigation in thirty days, they must delete the item from your report. Having that certified mail receipt keeps them on schedule. It gives you the legal leverage you need to force a quick response.

Keeping Your Own Paper Trail

Keep a copy of everything you send to the bureaus. This includes the letter itself, the copies of your evidence, and the certified mail receipt.

Store these in a safe place. If a bureau claims they never received your dispute, you can show them the delivery receipt. Having a complete paper trail protects your rights if you need to take further action later.

Understanding Your Rights Under the Law

You do not have to beg the credit bureaus to fix their mistakes. The law is on your side. The Fair Credit Reporting Act was created to protect everyday consumers from big data companies.

This law states that your credit report must be accurate, fair, and kept private. If a company reports false information about you, they are breaking the law.

Knowing this should give you the confidence to stand up for yourself. You are not asking for a favor. You are demanding that your legal rights be respected.

When you send a well-organized dispute with solid proof, the credit bureaus must contact the bank that reported the data. The bank then has to check their records. If the bank cannot find proof of the debt or the late payment, they must tell the credit bureau to delete it.

This process is highly effective because many older debts lack proper documentation. If a bank sold your debt to a collection agency, the paperwork is often lost in transition. If they cannot prove the debt belongs to you, it must come off your report.

This is how people often see their credit scores jump by fifty or even one hundred points in a month. By removing major negative items that cannot be proven, your score recovers its natural strength.

A Critical Update on Medical Debt Rules:

"While a federal court vacated the CFPB's official rule banning medical debt from credit reports in July 2025, the reporting landscape remains highly favorable for consumers. Currently, the three major credit bureaus (Equifax, Experian, and TransUnion) continue to voluntarily exclude all paid medical collections from your credit reports, regardless of the amount. Furthermore, any unpaid medical debts under $500 are also completely excluded from appearing on your report. If you spot a paid medical collection or an unpaid medical debt of less than $500 on your report, you can dispute it immediately, and the bureaus must remove it based on their established policies."

Keep moving forward with your plan. In the next section, we will look at what happens after you send your letters and how to handle their responses. Your journey to a better credit score has already started.

Mastering the Credit System: Advanced Moves to Protect Your Score

So, you have sent your first dispute letters via certified mail. Your journey to a clean credit file is moving forward, but you need to know how to handle the next phase of the game.

The credit bureaus do not always make things easy. They might send you a letter claiming your request is "frivolous" or ask for more proof to delay the process.

This is where advanced strategies come into play. Knowing how to counter their moves will help you keep control of your financial destiny.

+-----------------------------------------------------------+ | THE TWO ROUTES FOR A DISPUTE | +----------------------------+------------------------------+ | Standard Bureau Route | Direct Creditor Route | | (Letters to Equifax, etc.) | (Letters to the Bank/Lender) | +----------------------------+------------------------------+

Step 4: Actively Follow Up and Counter Bureau Delay Tactics

When you send a dispute, the bureau must verify the information with the original creditor. If they cannot verify it within thirty days, they must delete it.

However, credit bureaus often try to stall. They might send a generic letter asking you to verify your identity again, even if you already sent your documents.

Do not let this discourage you. This is a common tactic to see if you will give up.

How to Respond to a "Frivolous" Letter

If a credit bureau labels your dispute as frivolous, they are trying to push you away. They do this when they think you are using a commercial template from a cheap repair agency.

- Do Not Panic: This does not mean your dispute is over.

- Write a Quick Response: Send a short, firm letter stating that you are a consumer personally reviewing your own credit report.

- Re-Attach Your Proof: Send the exact same evidence again, along with your original certified mail receipt to show they had the files all along.

- Demand an Investigation: Remind them of their legal duty under the Fair Credit Reporting Act to investigate accurate claims.

Using the Power of the Consumer Financial Protection Bureau

If the credit bureau completely ignores your proof, you have a powerful ally. You can file an official complaint with a government agency called the Consumer Financial Protection Bureau (CFPB).

Credit Bureau Ignores You ---> File Complaint with CFPB ---> Bureau Responds Fast

The CFPB acts like a referee in a sports match. When you submit a complaint on their official website, the credit bureau has to answer to the government.

Most bureaus will quickly reinvestigate and resolve your issue once they see the CFPB is watching. It is a highly effective way to cut through the red tape.

When All Else Fails: Partnering with an FCRA Attorney

If both the credit bureaus and the creditor stubbornly refuse to correct a clear, documented error even after you have submitted your proof and filed a complaint with the CFPB, you have the legal right to sue under the Fair Credit Reporting Act.

The best part? You do not need thousands of dollars to hire help. Many consumer rights and FCRA attorneys work on a contingency fee basis. This means they do not charge you any upfront fees. If they win your case, the law requires the credit bureau or creditor to pay your attorney’s fees, and you may even be awarded statutory and punitive damages for the stress and financial harm their negligence caused you.

Step 5: Master the Art of Direct Debt Validation with Collection Agencies

Sometimes, the error on your report comes from a third-party collection agency. These agencies buy old debts for pennies on the dollar and try to collect the full amount.

They often do not have the original paperwork. If they do not have the paperwork, they cannot legally report the debt on your credit file.

You can send a Debt Validation Letter directly to the collection agency to stop this.

The Magic of Asking for Original Proof

Think of it like a substitute teacher trying to grade you on a test they did not administer. If they do not have the answer key or your paper, they cannot give you a grade.

[Collection Agency] -----> Demands Payment -----> [You] Demands Original Contract

|

v

No Contract = Account Deleted

When you write to a collection agency, ask them for three specific things:

- The original contract signed by you and the original lender.

- The complete payment history showing how they calculated the balance.

- Proof that they are licensed to collect debts in your state.

If they cannot provide these items within thirty days, they must remove the account from your credit report. Many agencies will simply delete the account because finding old contracts from years ago is too difficult for them.

Keeping Your Clean Credit Report Shining Long-Term

Getting your score up is a massive win, but keeping it high requires a simple strategy. You do not want to go through this stressful process again.

A healthy credit score is like a garden. It requires regular attention to prevent weeds from growing back.

Freeze Your Credit Files for Safety

One of the smartest moves you can make is to freeze your credit reports at all three bureaus. This is completely free and takes only a few minutes.

A credit freeze stops anyone from opening a new account in your name. If a thief tries to apply for a card using your social security number, the lender will reject the application instantly.

When you want to apply for a loan yourself, you can temporarily lift the freeze using a secure PIN. This simple habit keeps your credit file safe from identity theft and mixed-file errors.

Important Note: Avoid the Costly "Credit Lock" Trap

While managing your credit file, you will likely see advertisements from the credit bureaus pushing "Credit Locks." Do not confuse a credit lock with a credit freeze.

By federal law, a Credit Freeze is 100% free, easy to manage, and offers strong statutory protections. A Credit Lock, on the other hand, is a commercial product that bureaus often package into monthly subscription plans. Furthermore, locking your credit often requires you to sign a user agreement that waives your legal right to join a class-action lawsuit if a data breach occurs. Always choose the free, federally protected credit freeze over a commercial lock.

Set Up Soft-Pull Monitoring Alerts

You do not need to check your full reports every day. Instead, use a free credit monitoring service that uses soft-pull technology.

These services do not hurt your credit score when they check your file. They will send a text or email alert the moment a new account or change appears on your report.

If you see an unauthorized change, you can act immediately before it causes major damage. Early detection is the key to maintaining a perfect score.

Hidden Traps: The Five Biggest Mistakes to Avoid During Your Dispute

While disputing errors is a straightforward process, many people accidentally sabotage their own progress. Avoiding these common traps will save you time, money, and frustration.

Understanding these pitfalls helps you protect your hard work. Let us look at the five mistakes that trip up most consumers.

<div style="overflow-x: auto; margin: 20px 0;">

<table style="width:100%; border-collapse: collapse; font-family: sans-serif; text-align: center; border: 1px solid #ddd;">

<thead>

<tr style="background-color: #d9534f; color: white;">

<th colspan="2" style="padding: 12px; border: 1px solid #ddd; font-weight: bold;">CRITICAL DISPUTE MISTAKES TO AVOID</th>

</tr>

</thead>

<tbody>

<tr>

<td style="padding: 12px; border: 1px solid #ddd; width: 50%;"><strong>1. Disputing Online</strong><br><small>(Waives specific legal appeal rights)</small></td>

<td style="padding: 12px; border: 1px solid #ddd; width: 50%;"><strong>2. Sending Messy Letters</strong><br><small>(Leads to scanning errors by automated systems)</small></td>

</tr>

<tr style="background-color: #f9f9f9;">

<td style="padding: 12px; border: 1px solid #ddd;"><strong>3. Over-disputing Items</strong><br><small>(Triggers a 'frivolous' rejection flag)</small></td>

<td style="padding: 12px; border: 1px solid #ddd;"><strong>4. Throwing Away Records</strong><br><small>(Deletes your proof if error reappears later)</small></td>

</tr>

<tr>

<td colspan="2" style="padding: 12px; border: 1px solid #ddd;"><strong>5. Closing Old Accounts</strong><br><small>(Shortens credit history and hurts overall score)</small></td>

</tr>

</tbody>

</table>

</div>

Mistake 1: Disputing Your Errors Online

It is highly tempting to use the "Dispute" button on the credit bureau websites. It looks fast, easy, and modern, but it is a major trap.

When you dispute online, you often agree to terms that waive your right to appeal or sue if they make a mistake. Furthermore, the online system limits the amount of proof you can upload.

The system translates your dispute into a simple two-digit code. This removes the context of your story and makes it easy for their computer to reject your claim. Always write physical letters and send them via mail to keep your full legal rights.

Mistake 2: Sending Messy or Emotional Letters

When writing your letter, do not let your anger get the best of you. Writing things like "This is unfair and you are ruining my life" does not help your case.

The bureau employee reviewing your file is just doing a job. If your letter is hard to read or filled with emotional complaints, they may not understand what you want.

Keep your letter clean, neat, and typed if possible. Stick to the facts, list the account numbers clearly, and point directly to your evidence documents.

Mistake 3: Disputing True Negative Items as Errors

Some people try to use the dispute system to delete accurate negative items, like a bill they actually forgot to pay. This is a highly dangerous strategy.

The credit bureaus have smart systems that can detect when someone is lying. If you dispute a true negative item repeatedly without proof, they will label all your disputes as frivolous.

Once they do this, they will ignore your real disputes too. Only dispute items that are truly inaccurate, outdated, or unverified.

Mistake 4: Throwing Away Your Correspondence Records

When a dispute is resolved, the bureau will send you a letter showing the updates. Many people throw these letters away once they see their score go up.

This is a big mistake. Sometimes, deleted errors can accidentally reappear on your report due to a computer glitch.

If that happens, you need your old deletion letter to prove the bureau already agreed to remove the item. Keep a physical folder with all your credit dispute letters and results for at least several years.

Mistake 5: Closing Old Accounts Once the Dispute is Finished

If you successfully dispute a mistake on an old credit card, you might feel like closing that account forever. You might think, "I do not use this card anyway, so let us close it."

However, closing an old account can actually lower your credit score. The system looks at the average age of your accounts to calculate your score.

Older Accounts = Longer Credit History = Higher Credit Score

If you close an old card, you make your credit history look shorter. Keep those old, positive accounts open, even if you do not use them, to keep your score high.

Beyond Disputes: Positive Habits to Accelerate Your Credit Growth

Removing errors from your credit report is only half the battle. To truly accelerate your score's recovery and maintain it long-term, you should actively practice credit-building habits:

- Keep Utilization Low (Under 10%): Your credit utilization ratio—how much limit you use relative to your total credit limit—accounts for 30% of your FICO score. Try to pay down your balances before your monthly statement closing date so that a low balance is reported to the bureaus.

- Establish a Credit Builder Tool: If your credit history is thin, consider opening a secured credit card or a credit-builder loan. These accounts require a refundable deposit but report positive, on-time payments to all three major bureaus every month.

- Become an Authorized User: If you have a trusted family member with a long, flawless credit history on a specific credit card, ask to be added as an "authorized user" on that account. Their positive payment history on that card may be added to your own report, giving your score an extra boost.

Your New Financial Chapter Starts Today

Taking control of your credit score can feel like a daunting task, but you now have the knowledge to succeed. You do not have to accept the mistakes of a broken system.

By following this step-by-step guide, you can confidently stand up to the credit bureaus and demand accuracy. Every error you remove brings you one step closer to your financial goals.

Imagine the feeling of walking into a bank and knowing you will get approved for a mortgage or a car loan with the lowest rates. That peace of mind is worth the effort of writing a few letters.

Do not wait for a perfect moment to begin. Take your highlighted credit report, grab your proof documents, and write your first dispute letter today.

Your financial future is in your hands, and your journey to a better credit score starts with a single letter. You have the facts, you have the rights, and you have the power to make it happen.

Frequently Asked Questions (FAQ)

Q: How long does it take for my credit score to improve after a successful dispute?

A: Once a credit bureau removes or corrects an error, the update is reflected in your credit file almost immediately. However, it may take 30 to 45 days for your updated score to show up on third-party credit monitoring services, as they require time to sync with the major bureaus.

Q: What should I do if the credit bureau does not respond within the 30-day limit?

A: Under the Fair Credit Reporting Act (FCRA), if a bureau fails to investigate and respond within the legal timeframe (usually 30 days, or 45 days under specific conditions like using free annual reports), they are legally required to delete the disputed item. You should send a follow-up letter demanding immediate deletion, attaching your original Certified Mail receipt as proof of delivery.

Q: Can a deleted error reappear on my credit report later?

A: Yes, occasionally a creditor might accidentally re-report the same incorrect data. If this happens, the Fair Credit Reporting Act requires the credit bureau to notify you in writing within 5 business days of the reinsertion. You can easily get it removed again by sending them your previous dispute resolution letter showing they had already agreed to delete the item.

Disclaimer:

Please Read Carefully

The information provided in this article is for educational, informational, and entertainment purposes only. It does not constitute formal legal, financial, investment, or tax advice.

While we make every effort to ensure the accuracy, completeness, and timeliness of the information presented, credit laws (including the Fair Credit Reporting Act and FDCPA regulations) and credit bureau policies are subject to change. The strategies, templates, and steps outlined here are based on general consumer rights, but individual financial situations vary.

We do not guarantee any specific financial outcome, credit score increase, or the successful deletion of any negative items from your credit report. Credit repair outcomes depend entirely on the unique facts of your credit history and the validation provided by your creditors.

Before making any major financial decisions or pursuing legal action, we strongly recommend consulting with a certified financial planner, a qualified credit counselor, or a licensed attorney in your jurisdiction. Use of any information or templates provided in this article is solely at your own risk

"@context": "https://schema.org",

"@type": "FAQPage",

"mainEntity": [

{

"@type": "Question",

"name": "How long does it take for my credit score to improve after a successful dispute?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Once a credit bureau removes or corrects an error, the update is reflected in your credit file almost immediately. However, it may take 30 to 45 days for your updated score to show up on third-party credit monitoring services, as they require time to sync with the major bureaus."

}

},

{

"@type": "Question",

"name": "What should I do if the credit bureau does not respond within the 30-day limit?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Under the Fair Credit Reporting Act (FCRA), if a bureau fails to investigate and respond within the legal timeframe (usually 30 days, or 45 days under specific conditions like using free annual reports), they are legally required to delete the disputed item. You should send a follow-up letter demanding immediate deletion, attaching your original Certified Mail receipt as proof of delivery."

}

},

{

"@type": "Question",

"name": "Can a deleted error reappear on my credit report later?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Yes, occasionally a creditor might accidentally re-report the same incorrect data. If this happens, the Fair Credit Reporting Act requires the credit bureau to notify you in writing within 5 business days of the reinsertion. You can easily get it removed again by sending them your previous dispute resolution letter showing they had already agreed to delete the item."

}

}

]

}