Why a High Debt-to-Income Ratio Keeps Holding You Back

You work hard. Your paycheck lands, and somehow it's already spoken for before you even open your banking app.

Rent, a car payment, two credit cards, maybe a student loan you've been chipping away at for years. By the time you add it all up, there's barely anything left.

Then you apply for a loan or try to refinance something, and the lender says one word that stops you cold: denied. Not because of your character, your work ethic, or your intentions. Because of a single ratio they barely explained to you.

You leave that meeting replaying every responsible thing you've done in your head. You've paid your bills on time. You haven't missed a payment in years. None of that seemed to matter once this one unfamiliar number entered the conversation.

Your debt-to-income ratio, or DTI, is simply the percentage of your monthly income that goes toward debt payments. But when it's too high, it can quietly block doors you didn't even realize were locked.

Why This Number Trips Up So Many People

Most people have never been taught what DTI actually measures or how lenders use it. That gap in knowledge causes real damage.

- They focus only on their credit score, assuming a good score automatically means a good DTI, when the two measure completely different things.

- They guess at their ratio instead of calculating it, so they apply for loans they were never going to qualify for in the first place.

- They pay off the wrong debts first, chasing the biggest balance instead of the payment that actually drags their ratio down fastest.

- They take on new debt while trying to fix the problem, like financing a new phone or car, without realizing it cancels out their progress.

- They don't realize income matters just as much as debt, so they only attack one half of the equation.

None of this happens because someone is bad with money. It happens because nobody sits you down and explains how the math actually works, step by step, in plain language.

The Quiet Weight This Puts on You

A high DTI doesn't just block loan approvals. It chips away at how you feel day to day.

- You start avoiding conversations about big purchases, even ones you genuinely need to make.

- You feel a flash of dread every time an unexpected bill shows up in the mail.

- You compare yourself to coworkers or friends who seem to "have it together," without knowing their real numbers.

- You begin to believe a denial says something about your worth, instead of just reflecting a math problem you haven't solved yet.

- Sleep gets harder when your mind keeps replaying the same monthly math at 2 a.m.

Take Marcus, an electrician in Georgia. He earns a solid income, but between a truck payment, two credit cards, and a personal loan from a few years back, his DTI sat above 48%.

He applied for a mortgage and got denied, even though his credit score was respectable. The loan officer mentioned his ratio almost in passing, like it was obvious, but Marcus had never even heard the term before that meeting.

He left that appointment feeling like a failure, when really, he just needed a clear plan. That's the gap this guide is built to close.

A few months later, Marcus sat down and ran the actual numbers for the first time. He found that two smaller debts, a personal loan and a store credit card, were responsible for nearly $400 of his monthly obligations combined, despite carrying a fraction of his total balance. Clearing those two accounts first, while holding off on financing anything new, brought his ratio down enough to requalify within half a year.

A high DTI isn't a life sentence. It's a number you can move, often faster than people expect once they understand exactly which levers to pull. Let's walk through the first three moves that make the biggest difference.

Your First Three Moves to Bring Your Ratio Down

Lowering your DTI comes down to two forces: how much you owe each month, and how much you earn. Let's tackle both, starting with the step almost everyone skips.

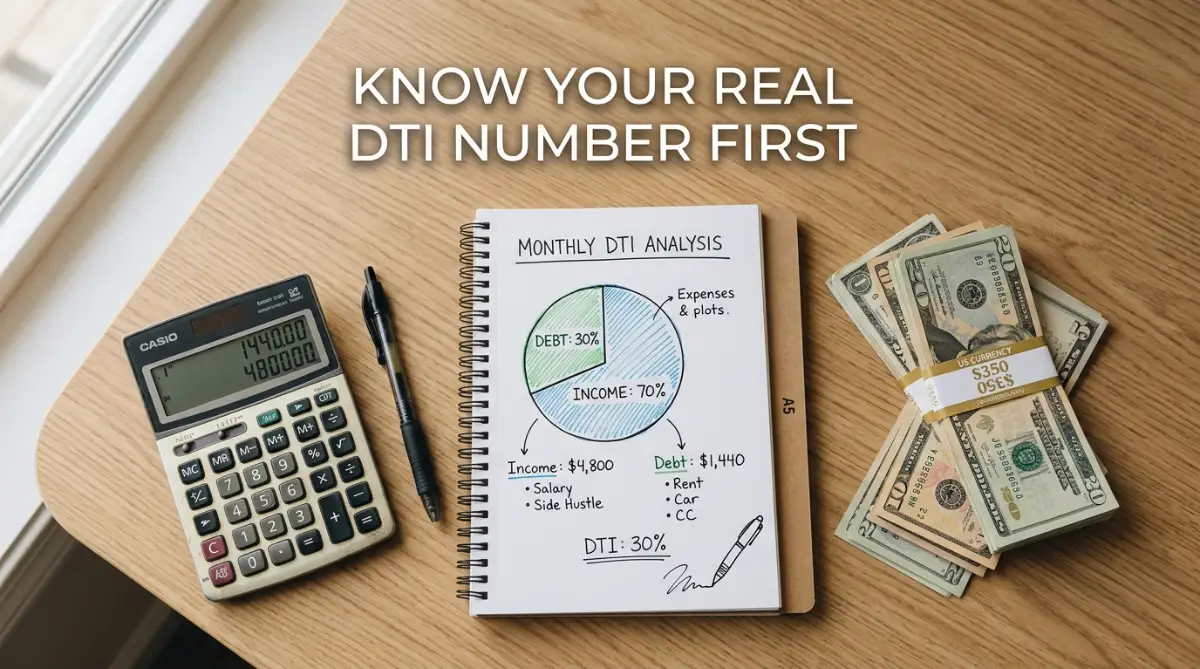

Step One: Find Your Real Number Before You Guess at Anything

You can't fix a number you've never actually calculated. Add up every required monthly debt payment, then divide that total by your gross monthly income.

Include things like:

- Minimum credit card payments (not your full balance, just the minimum due).

- Car loans, personal loans, and student loan payments.

- Your rent or mortgage payment, including property tax and insurance if you own.

- Child support or alimony, if it applies to you.

You can use a free DTI calculator to double-check your math, or just do it by hand with a calculator and five minutes of focus.

Here's a quick example. Say your monthly debts add up to $2,200, and your gross monthly income is $5,500. Divide $2,200 by $5,500, and you get a DTI of 40%, a number many lenders would consider on the higher side.

Knowing this exact figure changes everything. It turns a vague feeling of "I owe too much" into a specific target you can actually move.

Step Two: Attack the Debt That Moves the Needle Fastest

Here's something most people get backward. The debt with the highest balance isn't always the one hurting your ratio the most.

Your DTI cares about your monthly payment, not your total balance. A $200-per-month payment on a $2,000 balance affects your ratio the same as a $200-per-month payment on a $20,000 balance.

This means paying off smaller debts with disproportionately high monthly payments can drop your ratio faster than chasing your largest balance first. This is exactly the logic behind the debt snowball method, where eliminating whole payments, not just balances, creates momentum you can actually measure.

Picture two debts: a $3,000 personal loan with a $250 monthly payment, and a $9,000 car loan with a $180 monthly payment. Paying off the personal loan first removes $250 from your monthly debt total, a bigger and faster win for your DTI than the car loan would offer.

Think of it like clearing a clogged sink. You don't always reach for the biggest piece of debris first. Sometimes the small clog closest to the drain is what's actually stopping the water from flowing, and clearing it makes the biggest visible difference right away.

This doesn't mean ignore your larger balances entirely. It means sequence your effort so the first few months show real, visible movement, which keeps you motivated to finish the rest of the plan.

Step Three: Stop Adding New Debt While You Work the Plan

This step sounds obvious, but it trips up more people than you'd expect.

Every new debt payment you add cancels out progress you've already made. Financing a couch, opening a new credit card for a discount, or adding a second car payment can quietly undo weeks of hard work.

A simple way to stay on track:

- Pause any "buy now, pay later" plans until your ratio improves.

- Use cash or a debit card for discretionary spending during this period.

- If a real emergency comes up, look at your savings before reaching for a credit card.

Building even a basic budget you can stick to makes this step far easier, since you'll know exactly how much breathing room you have before you're tempted to add anything new.

A Few Things People Get Wrong About DTI

Before we move into the action steps, let's clear up some confusion that trips up a lot of borrowers.

"My credit score is good, so my DTI must be fine too." These are two completely separate measurements. You can have an excellent credit score built on years of on-time payments while still carrying a DTI that's too high for a lender's comfort, simply because your income hasn't kept pace with your monthly obligations.

"Paying off debt always lowers my DTI right away." Mostly true, but not always immediately. If you pay off a credit card but keep the account open with a zero balance, your DTI improves the moment that payment posts, since the minimum due drops to nothing.

"A DTI under 50% means I'll get approved." Not necessarily. Different loan types have different ceilings. Conventional mortgages often want a back-end ratio under 36% to 43%, while some personal loans tolerate a higher number.

"Income from a side gig doesn't count toward my DTI." It actually can, as long as you can document it consistently, usually with a couple of years of tax returns or pay stubs showing the extra income is stable rather than a one-time bonus.

Why These Three Moves Work Together

Calculating your real number tells you exactly where you stand. Targeting the right debts first gets you the fastest visible progress. Avoiding new debt protects every gain you make along the way.

This isn't about depriving yourself for years. It's about being deliberate for a focused stretch of time, long enough to move your ratio into a range that actually opens doors, whether that door is a mortgage, a car loan, or simply peace of mind every time you check your bank account.

Borrowers who follow this order, instead of randomly throwing money at whatever debt feels most urgent, tend to see real movement in their ratio within just a few months. The number isn't fixed. It responds directly to the choices you make starting today.

If you want a deeper technical breakdown of how lenders weigh DTI across different loan types, Experian's guide to reducing your ratio before applying for a loan is worth bookmarking, especially if a mortgage or auto loan is part of your near-term plans.

In the next part of this guide, we'll cover advanced strategies for boosting the income side of the equation, how to keep your ratio low for the long run, and the mistakes that quietly sabotage progress for people who are otherwise doing everything right

Pushing Your Ratio Down Faster With the Income Side of the Equation

Paying down debt is only half the equation, and it's the half most articles focus on. The other half, your income, gets ignored far more often than it should.

A lot of borrowers spend months cutting expenses to the bone while never touching the numerator's twin: the bottom half of the fraction. Both sides matter equally, even though only one of them usually gets any attention.

Document Every Dollar of Income, Not Just Your Paycheck

Lenders don't automatically know about income beyond your main job. If you don't document it, it doesn't count toward your DTI, no matter how real that money is to you.

This includes things people often forget to report:

- Freelance or gig income, as long as you can show roughly two years of consistent earnings.

- Rental income from a property you own, supported by a lease agreement.

- Regular bonus or commission income, if your employer can confirm the pattern.

- Alimony or child support you receive, if you choose to include it.

A nurse named Priya picked up two weekend shifts a month at a second facility to bring in extra cash on top of her regular hours. After eight months of consistent pay stubs, that extra income became something a lender could actually count, shifting her ratio in a way that cutting expenses alone never would have.

Refinance or Restructure Existing Debt to Lower Monthly Payments

Here's a strategy most people never consider. You don't always need to pay off debt to lower your DTI. Sometimes you just need to restructure how you pay it.

A few ways this plays out in real life:

- Refinancing a car loan to a longer term can lower your monthly payment, even though you'll pay more interest over time.

- Consolidating several credit cards into one fixed personal loan often reduces your total required monthly payment compared to scattered minimum payments.

- Refinancing student loans, when the math works in your favor, can stretch payments out and free up monthly cash flow.

This trade-off matters, so think it through carefully. Lowering your monthly payment by extending your term can help you qualify for a loan today, but it usually means paying more in total interest over the life of that debt.

Think of it like loosening your belt one notch for a season versus going on a strict diet forever. Sometimes the short-term adjustment gets you through a specific goal, like qualifying for a mortgage, even if it's not your permanent long-term plan.

Ask Creditors Directly About Lower Monthly Payments

Most people never think to simply ask. Some creditors will lower your minimum payment or adjust your terms if you call and explain your situation honestly.

This works especially well with medical debt, where many providers offer interest-free payment plans that aren't advertised anywhere on their website. A $300 monthly medical bill turned into a $75 monthly plan can shift your DTI noticeably, without touching your other debts at all, and without a single dollar of interest added on top.

Credit card issuers sometimes offer hardship programs too, temporarily lowering your interest rate or minimum payment if you've been a customer in good standing for a while. It costs nothing to ask, and the worst outcome is simply hearing no, which leaves you exactly where you already were.

Build a Habit That Keeps Your Ratio Low for Good

Getting your DTI down once is a win. Keeping it down is the real goal, and that takes a different kind of habit than the initial push.

A few practices that protect your progress over time:

- Recalculate your DTI every few months, not just when you're about to apply for something. This keeps you aware before a problem creeps back in.

- Treat new debt as a deliberate decision, never an impulse. Ask yourself how any new payment will affect your ratio before you sign anything.

- Keep a small buffer fund so an unexpected expense doesn't force you back onto a credit card. Even a modest emergency fund built over a few months can absorb a surprise bill without undoing your progress.

- Revisit your budget seasonally, since expenses shift with the time of year, and a budget that worked in spring might not hold up during the holidays. Tracking your daily spending for even two weeks each season makes these shifts easy to catch before they snowball into a missed payment.

- Celebrate the small drops. A ratio moving from 44% to 38% is real progress, even if it's not yet where you ultimately want it to land.

Borrowers who build these habits into their normal routine, rather than treating DTI as a one-time fix, tend to stay in a healthy range for years afterward. The goal isn't a single good month. It's a number that stays low because your habits quietly support it.

The Slip-Ups That Quietly Undo Real Progress

Even people doing most things right can trip over a handful of common mistakes. Spotting them early means you can avoid losing momentum you worked hard to build.

Mistake One: Closing Old Accounts the Moment You Pay Them Off

It feels satisfying to close a credit card the second the balance hits zero. Closing accounts doesn't directly raise your DTI, but it can shrink your available credit and complicate your overall credit profile at the worst possible time.

A safer move is keeping the account open with a zero balance, especially if it carries no annual fee. Think of an old, paid-off card less like clutter to throw away and more like a quiet asset sitting in the background of your credit file.

Mistake Two: Forgetting Irregular or Co-Signed Debt

Plenty of people forget that a co-signed loan, even one someone else pays, still shows up on their credit report and counts toward their DTI.

Pull your full credit report and account for every single obligation tied to your name, not just the ones you're actively paying yourself.

A common scenario looks like this: you co-signed a $15,000 auto loan for a sibling years ago. They've made every payment on time, but that $280 monthly obligation still sits on your credit report, quietly inflating your ratio every time a lender pulls your file, whether you remember signing for it or not.

Mistake Three: Financing a Big Purchase Mid-Plan

Buying a new car or financing furniture while actively trying to lower your DTI can erase months of progress in a single afternoon.

If a purchase isn't urgent, delay it until after your ratio reaches your target range. A few months of patience protects everything you've already built.

Imagine spending four months paying down a credit card, only to finance a $2,500 living room set the week before you planned to apply for a mortgage. That new $120 monthly payment can be the exact difference between an approval and a denial letter you weren't expecting.

Mistake Four: Tracking Total Debt Instead of Monthly Payments

This mistake quietly misleads people about where they actually stand. Paying down $5,000 on a large loan can feel like major progress, but if your monthly payment barely changes, your DTI barely moves either.

Always check the monthly payment impact of any extra payment, not just the satisfaction of a smaller total balance.

Mistake Five: Letting Undocumented Income Sit Unused

If you've picked up steady freelance work or a side job but never report it consistently, a lender can't factor it into your ratio at all.

Start saving pay stubs, invoices, or bank deposit records now, even if you're not applying for anything yet. Two years of clean documentation can completely change your approval odds later.

What These Mistakes Actually Cost You

None of these slip-ups feel dramatic in the moment. Together, they can stall progress for months without you realizing why your ratio isn't moving the way you expected, even when you feel like you're doing everything right on paper.

A single mid-plan car purchase can undo six months of careful debt payoff in one signature. Forgetting a co-signed loan can mean applying for a mortgage with a ratio that's higher than you believed, leading to an unexpected denial.

The good news is that every mistake on this list is completely avoidable. None of them require financial expertise, just a habit of double-checking before you act on a big decision, especially one that involves signing anything new.

Your Ratio Is a Number You Control, Not a Verdict on You

A high debt-to-income ratio can feel like a label stuck to your financial life. It isn't. It's a number built from specific, fixable choices, and you now know exactly which ones matter most.

You know how to calculate your real ratio, attack the right debts first, document every dollar of income, and avoid the mistakes that quietly stall other people's progress.

Pick one move from this guide and start today. Maybe it's calculating your real DTI for the first time this evening. Maybe it's pulling your credit report to check for a forgotten co-signed loan.

Marcus eventually requalified for his mortgage. Priya's extra shifts became real, documented income that lenders could count. Neither of them needed a financial degree, just a clear order of steps and the patience to follow them.

That same clear path is sitting in front of you right now. The number on your credit file today isn't the number you're stuck with tomorrow, and every small step you take starting now moves you a little closer to the range you're actually aiming for.

None of this requires perfection. Some months will move faster than others, and that's normal. What matters is that you're no longer guessing, reacting to a denial letter, or wondering why a number you'd never even calculated kept showing up at the worst possible moments.

You already have the order of operations now: calculate, target the right debts, document your income, restructure where it makes sense, and protect your progress once you get there. That's a complete plan, not a collection of scattered tips, and it's one you can start working through today.