The Hidden Struggles of Getting a Personal Loan: Why It Feels So Hard

Imagine waking up to a sudden financial emergency that you did not see coming. Maybe your car broke down on your way to work, or a medical bill arrived in your mail.

You check your bank account, and your heart sinks because the funds are not there. The panic immediately sets in, and you feel a heavy weight on your chest.

This is the reality for millions of people who need quick financial help but do not know where to turn. You need money fast, but the thought of asking a bank makes you feel incredibly anxious.

You want a simple solution, but the financial world feels like a maze designed to keep you out. The confusion and fear of getting rejected can keep you awake all night.

Unfortunately, finding clear and honest help online is much harder than it should be. Many people fall into deep financial traps because they do not have the right guidance.

- Misleading online ads promise instant approval with no credit check, but they hide massive interest rates that ruin your finances.

- Desperate applicants apply to five different lenders at the same time, which damages their credit scores instantly.

- Unclear loan terms make it very hard for you to understand the actual cost of borrowing the money.

- Predatory lenders target people who are stressed, pushing them into loans they can never afford to pay back.

- Confusing bank jargon leaves you feeling lost and embarrassed to ask basic questions about the process.

This constant worry and confusion do more than just hurt your wallet. The struggle to find a safe loan can take a massive toll on your everyday life.

- The constant fear of rejection makes you feel like a failure, even though your financial situation is not your fault.

- High levels of stress spill over into your family life, causing arguments and sleepless nights with your loved ones.

- Endless phone calls from pushy salespeople can make you feel targeted and unsafe in your own home.

- A feeling of helplessness lowers your self-confidence, making you believe you will never get out of this tight spot.

- The loss of mental peace stops you from focusing on your job and enjoying the simple moments of your day.

Your Step-by-Step Educational Guide to Loan Preparation

Getting a personal loan does not have to be a scary or confusing experience. If you prepare correctly, you can walk into any bank or apply online with complete confidence.

We have built this simple guide to help you take back control of your financial future. Let us walk through the first three steps together so you can get approved without the stress.

Step 1: Check and Improve Your Credit Score First

Before you write your name on any application, you must know your credit score. Your credit score is like a financial report card that tells lenders how safely you manage your money.

Lenders look at this three-digit number to decide if they can trust you to pay them back. If your score is high, banks will welcome you with low interest rates and great terms.

If your score is low, they might reject your application or charge you very high fees. This is why checking your score is the absolute first thing you must do.

How a Single Score Changes Your Financial Reality

Let us look at a simple story to see how much your credit score actually matters. Imagine two friends, Sarah and John, who both want to borrow ten thousand dollars for a home project.

Sarah has spent years paying her bills on time, and her credit score is a strong 760. The bank happily offers her a personal loan with a low 6% interest rate.

John has a few missed payments from his past, and his credit score sits at a low 580. The bank views John as a high-risk borrower and offers him the same loan but at an 18% interest rate.

Because of his score, John will end up paying thousands of dollars more than Sarah for the exact same amount of money. This real-life example shows why a good score is your best tool to save cash.

How to Access Your Credit Report for Free

You do not need to pay expensive companies to see your credit history. You can easily get a free copy of your credit report online once every year from major credit bureaus.

When you get your report, do not just look at the final score at the top. Read through every single line to make sure all the information listed is correct.

Look for accounts you do not recognize or late payments that you actually paid on time. Mistakes happen more often than you think, and they can drag your score down without your knowledge.

Simple Actions to Raise Your Score Quickly

If your credit score is not where you want it to be, do not lose hope. You can start raising your score today with a few simple and smart habits.

First, make a commitment to pay every single bill on time, even if you only pay the minimum amount. Late payments are the single biggest factor that hurts your credit score.

Second, try to pay down your current credit card balances as much as possible. Keeping your card balances below 30% of your total limit shows lenders that you do not rely too heavily on borrowed money.

Finally, do not apply for any new credit cards or loans right before you apply for your personal loan. Every application triggers a check on your credit file, which can temporarily lower your score.

Step 2: Calculate and Lower Your Debt-to-Income Ratio

Once you know your credit score, the next step is to look at your Debt-to-Income (DTI) ratio. Lenders use this simple calculation to see if you have enough breathing room in your budget to afford a new payment.

Your DTI ratio compares how much money you owe every month to how much money you earn. If too much of your income already goes toward debts, lenders will worry that you cannot handle a new loan.

Understanding the Simple Math Behind Your DTI

Calculating your DTI ratio is very easy, and you can do it right now at your kitchen table. First, add up all your monthly debt payments, including credit cards, car loans, and student loans.

Do not include living expenses like groceries, utilities, or gas in this specific calculation. Next, take your gross monthly income, which is the amount of money you earn before taxes are taken out.

Now, divide your total monthly debt by your gross monthly income to get a percentage. For example, if you pay one thousand dollars in debts and earn three thousand dollars, your DTI is 33%.

The Analogy of the Weight Limit on a Bridge

To understand why banks care about this ratio, think of your monthly income as a small wooden bridge. Your current monthly bills are like heavy trucks that are already driving across that bridge.

If you have too many heavy trucks on the bridge at the same time, the wood will begin to bend and crack. If you try to drive one more truck across, the entire bridge might collapse into the water.

A lender wants to make sure your financial bridge is strong enough to support another truck. They want to see plenty of empty space on that bridge before they agree to give you more money.

What Is the Ideal DTI Ratio for Fast Approval?

Generally, lenders prefer to see a DTI ratio that is 36% or lower. A ratio this low tells the bank that you have plenty of extra money left over after paying your bills.

If your ratio is between 37% and 43%, you can still get approved, but you might face stricter rules. If your ratio is above 43%, most traditional banks will view your situation as too risky.

Knowing your ratio before you apply helps you see your financial health exactly how the bank sees it.

Easy Ways to Improve Your Ratio This Week

If your DTI ratio is too high, you have two basic ways to fix it before you apply. You can either lower your monthly debt payments or find ways to increase your monthly income.

Start by targetting your smallest credit card balances and paying them off completely to eliminate those monthly payments. Even getting rid of a small fifty-dollar monthly payment can help your ratio.

If you cannot pay down your debts quickly, consider taking on a temporary side job to bring in extra cash. Increasing your income, even by a small amount, immediately lowers your ratio and makes you look much safer to lenders.

Step 3: Decide on Your Exact Loan Amount and Monthly Budget

The third step in your checklist is to figure out exactly how much money you need to borrow. It is very tempting to borrow extra cash "just in case," but this is a trap you must avoid.

Borrowing more money than you need means you will pay interest on cash you did not actually use. You must be precise and honest with yourself about your financial needs.

Why Borrowing Too Much Can Break Your Budget

Let us look at another real-life scenario to see why borrowing too much is dangerous. Imagine you need five thousand dollars to fix a broken pipe in your bathroom.

The lender tells you that you qualify for a ten-thousand-dollar loan instead. You think it would be nice to have the extra five thousand dollars to buy new furniture and go on a small trip.

However, that extra money comes with a price, and your monthly payment will now double. If you experience a tough month later on, that high payment could push you into deep financial trouble.

Stick to your original goal and only borrow the exact amount required to solve your immediate problem.

How to Use a Loan Calculator Like a Professional

Before you sign any contract, you should use an online loan calculator to test different scenarios. These free tools let you enter different loan amounts, interest rates, and payback terms.

You can see exactly how much you will pay every single month and how much total interest you will pay over time. Play around with the numbers until you find a monthly payment that fits comfortably into your budget.

Never guess what your payment will be because even a small interest rate change can alter your monthly bills.

Finding the Balance Between Short and Long Terms

When choosing your loan term, you must balance your monthly payment with the total cost of the loan. A shorter term, like two years, means you will have higher monthly payments.

However, you will pay off the debt quickly and pay very little interest over the life of the loan. A longer term, like five years, will give you low, comfortable monthly payments.

The downside is that you will pay interest for a much longer time, making the loan much more expensive in the long run. Choose the shortest term that you can comfortably afford without straining your monthly budget.

Hidden Fees to Watch Out For in the Fine Print

When you apply for a personal loan, the interest rate is not the only cost you need to consider. Lenders often add hidden fees that can make your loan much more expensive than you think.

- Origination fees are charges that lenders take out of your loan amount before they give you the money. If you borrow five thousand dollars, they might take out two hundred dollars as a fee, leaving you with less cash than you needed.

- Prepayment penalties are fees some lenders charge if you try to pay off your loan early to save on interest. You should always look for a lender that does not punish you for being responsible and paying early.

- Late payment fees are charged if you miss your payment date, and these fees can quickly pile up and hurt your credit score.

- Annual fees are yearly charges that some banks require just for keeping your loan account open.

Always read the fine print and ask the lender for a full list of fees before you accept any offer. Knowing these details keeps you safe and ensures you do not get any bad surprises down the road.

Creating a Stress-Free Application Experience

By following these first three steps, you are already far ahead of most people who apply for loans. You know your credit score, you understand your budget, and you know exactly how much you need to borrow.

This preparation protects you from making emotional decisions that could hurt your financial future. You do not have to feel powerless when dealing with big banks and lenders.

With the right knowledge, you can make decisions that protect your family and your peace of mind. In the next part of our guide, we will look at how to gather your documents and choose the right lender.

Taking Control of the Loan Process: Expert Secrets for Success

Preparing yourself before applying for a loan is like packing a bags before a long journey. If you do not have the right items, you will face major delays along the way[1].

Taking charge of your financial situation will help you get approved quickly and easily[1]. We will now explore the next step-by-step secrets that the smartest borrowers use to save money and stress.

Step 4: Build a Perfect Document Folder to Speed Up Your Approval

Lenders want to see proof of your financial situation before they can trust you with their money[2]. Gathering these documents early shows the bank that you are organized, responsible, and serious about your request.

According to a detailed guide on applying for a personal loan from Investopedia, having your papers ready can prevent weeks of back-and-forth communication with the bank. If you miss even one small form, your application could sit on a desk for several days without any action.

Why Paper Preparation Matters

Let us compare two different borrowers, Mike and Sarah, to see how preparation changes things. Mike decided to apply for a loan on a whim after seeing an online ad.

He did not bring his tax papers or his pay slips to the bank because he thought they could just look up his name. The banker had to send him home to look for his records, which took Mike three days to find.

Sarah, on the other hand, spent one evening gathering all her documents into a single neat folder on her computer. She submitted everything on her first attempt and had her cash in her bank account within forty-eight hours.

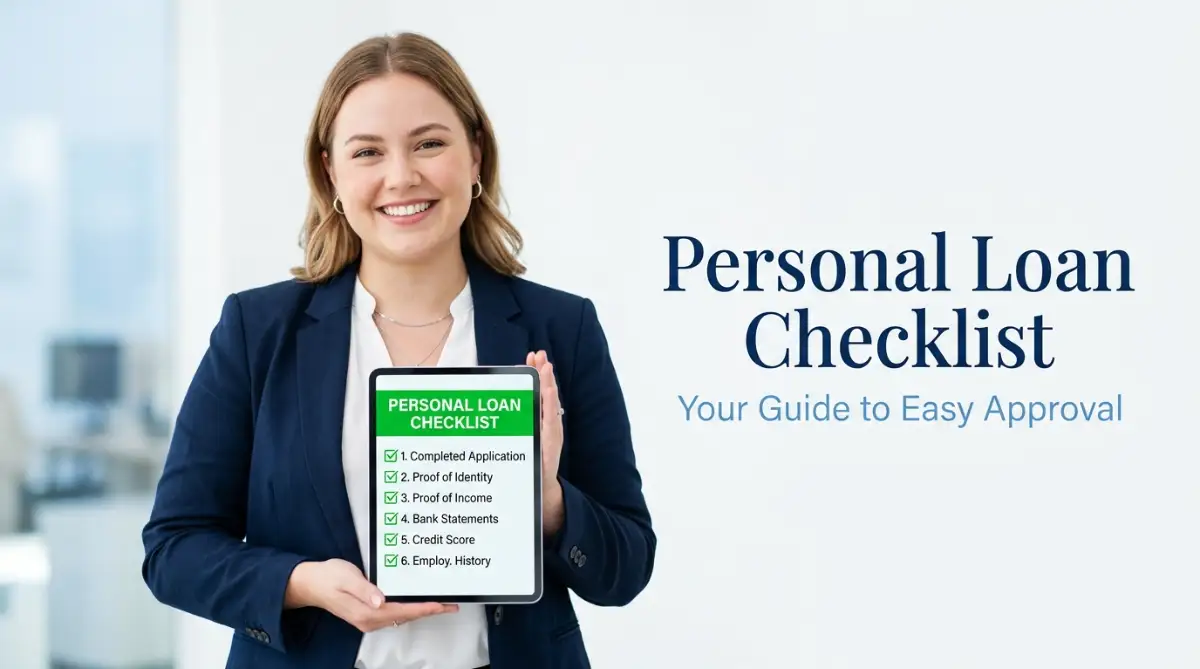

The Complete Paperwork Checklist

To make sure you get approved as fast as Sarah, you should create your own document folder today. Most traditional banks and online lenders will ask for the exact same pieces of information.

- Proof of your identity, which includes a valid government-issued photo ID like a driver's license or passport[3].

- Proof of your home address, which can be shown using a recent utility bill or a lease agreement in your name[3].

- Proof of your steady income, including your last three pay slips or tax files if you work for yourself[2].

- Recent bank statements from the last ninety days to prove you have a stable flow of cash coming in and out[2].

- A signed letter from your employer confirming that you are currently employed and holding a stable position[2].

Having both digital PDFs and physical copies of these files ready will make the entire process incredibly smooth.

Step 5: Shop Around and Compare Multiple Lenders

Many people make the massive mistake of accepting the very first loan offer they receive. This is like buying the first car you see on a lot without checking any other dealerships.

Different banks charge different interest rates and fees, even for the exact same borrower[2]. By looking at multiple options, you can find a deal that fits your monthly budget perfectly.

The Consumer Financial Protection Bureau's guide on loan options points out that shopping around for a loan can save you hundreds of dollars in interest charges over time[4]. Lenders are competing for your business, and you should use that to your advantage.

Choosing the Right Type of Financial Institution

You have several different types of lenders to choose from when you need a personal loan. Each option has its own set of pros and cons depending on your credit history.

Traditional banks are great if you already have an established relationship with them and have an excellent credit score[1]. They often offer highly competitive rates to their loyal customers but have a very slow approval process.

Credit unions are non-profit organizations that are owned by their members, which means they can offer lower interest rates. They are usually much more willing to work with borrowers who have less-than-perfect credit.

Online lenders are incredibly fast and convenient, often letting you apply and get approved directly from your smartphone[1]. However, you must watch out for higher fees and check their reviews to make sure they are trustworthy[1].

Comparing the Annual Percentage Rate Instead of the Interest Rate

When you are looking at different loan offers, do not just compare the basic interest rates. Instead, you should always look closely at the Annual Percentage Rate (APR)[1].

The basic interest rate only tells you how much it costs to borrow the money each year. The APR is a much more honest number because it includes both the interest rate and any extra fees the lender charges[5].

If a bank offers you a low interest rate but charges a massive sign-up fee, the APR will be high. Always use the APR as your main point of comparison to see the true cost of the loan.

How to Handle Your Active Loan and Protect Your Wealth

Getting your loan approved is a great feeling, but your journey does not end when the money lands in your bank. Managing your monthly payments responsibly is how you protect your credit score for the future.

Before you spend a single dollar of your new loan, you must adjust your daily spending habits. Learning how to create a real budget that stops the financial bleeding is the best way to ensure you always have enough cash to cover your payments.

Setting Up Automated Tools for Peace of Mind

The easiest way to make sure you never miss a payment is to set up automatic transfers with your bank. You can schedule the loan payment to leave your account the day after you get paid.

This simple habit keeps you safe from late fees and protects your credit score from accidental damage[1]. Many online lenders will even give you a small interest rate discount if you agree to use auto-pay.

Building a Safety Net for the Unexpected

While you are paying off your new debt, you should also focus on saving a small amount of money for yourself. Having a small cash buffer will stop you from needing to borrow money again when your next emergency happens.

We highly recommend learning how to build an emergency fund from scratch even when your budget feels incredibly tight. Saving just twenty dollars a week can quickly grow into a solid safety net over time.

You can also start tracking daily spending to stop money leaks so you can find extra money to pay down your loan early. Every extra dollar you pay toward your principal balance reduces the total interest you will owe.

Dangerous Pitfalls to Avoid When Borrowing Money

Getting a personal loan can be a highly effective way to solve a temporary financial problem. However, if you are not careful, you can make costly mistakes that will hurt your budget for years.

Many people rush into the borrowing process because they are stressed and need quick cash[1]. By learning about these major traps now, you can keep your finances safe and secure.

1. Falling for the Low Monthly Payment Trap

Lenders love to show you how low your monthly payments can be if you choose a longer loan term. They do this because they want you to focus on the small monthly number instead of the total cost.

A low monthly payment usually means you are stretching the loan over five to seven years. During that long time, the interest charges will build up and make the loan incredibly expensive.

Always calculate the total payback amount by multiplying your monthly payment by the number of months in the term. You might find that a low payment actually makes you pay double the amount you borrowed.

2. Ignoring Your Credit Score Until the Last Minute

Many people submit loan applications without ever looking at their own credit files. This is highly risky because errors on your credit report can cause instant rejection[2].

Before you apply, you should find out how to improve your credit score quickly by disputing errors on your report. Fixing these small mistakes can lift your rating and help you qualify for much lower interest rates[1].

Taking the time to check your file first can save you thousands of dollars over the life of your loan.

3. Borrowing Money for Wants Instead of Real Needs

A personal loan is an excellent tool for emergencies, medical bills, or consolidating high-interest debt[4][5]. It is not a good tool for buying expensive electronics, going on vacations, or funding a luxury lifestyle.

Borrowing money to buy things that lose value quickly is a guaranteed way to build bad financial habits. If you want to make a fun purchase, it is always better to save up cash over time.

Reserve personal loans strictly for situations where the money will improve your financial life or solve a critical crisis.

4. Overlooking the Impact of Multiple Hard Enquiries

Every time you submit an official application for a loan, the lender performs a deep check on your credit history. This check is called a hard inquiry, and it will temporarily lower your credit score[1].

If you apply to four or five different banks in a single week, your credit score will drop significantly. Other lenders will see this sudden drop and assume that you are desperate for cash or in deep trouble.

Instead of applying everywhere, use pre-qualification tools that only perform soft credit checks first. This allows you to see your estimated rates without hurting your rating[1].

5. Forgetting to Read the Terms on Prepayment Fees

Some lenders do not want you to pay off your debt early because they lose out on interest payments. To prevent this, they add prepayment penalties to the fine print of your contract.

If you get a bonus at work or find extra cash, you should be able to pay off your loan instantly without any fees. Always ask the loan officer if there are any charges for paying off the balance early.

Avoid any lender that tries to lock you into a payment plan by punishing your responsible behavior.

Your Path Forward to Financial Freedom and Peace

Taking out a personal loan is a major financial step, but it does not have to be a source of stress or anxiety. By following a clear checklist, you can make smart decisions that protect your family and your future[1].

Remember that you are in complete control of this process from start to finish. You have the power to check your credit score, calculate your budget, and compare lenders to find the best deal[1].

Summary of Your Action Plan

To help you get started today, here is a quick summary of the steps we have covered:

- Check your credit history for any mistakes and take quick steps to raise your score[1][2].

- Calculate your debt ratio to see exactly how much cash you have left over each month[2].

- Pick a sensible amount to borrow and avoid the temptation to take extra cash.

- Gather all your paperwork into a neat digital folder before you contact any bank[2].

- Compare the APR of multiple lenders to find the absolute lowest overall cost[1].

Take Your First Small Step Today

You do not have to do everything at once to make meaningful progress. Start by taking just ten minutes tonight to check your credit score for free[1].

That single small action will show you exactly where you stand and give you the confidence to move forward. Financial peace of mind is built one simple, smart decision at a time.

You have the knowledge, you have the tools, and now you have a clear roadmap to guide you. Take a deep breath, trust your preparation, and take charge of your financial journey today.