Why Applying for a Personal Loan Feels More Stressful Than It Should

You finally decide to apply for a personal loan. Then the questions start piling up in your head.

Which lender do you even pick? What documents do they need? Will they say no after you've already spent an hour filling out a form?

This is the exact moment where a lot of people freeze. The application itself isn't hard. What makes it stressful is not knowing what to expect.

So you open five browser tabs, read three conflicting articles, and end up more confused than when you started.

One site tells you to apply everywhere at once to "see what sticks." Another warns that doing exactly that will tank your credit score. By the time you've read a fourth article, you're not sure who to trust anymore, so you close the laptop and tell yourself you'll deal with it tomorrow.

Why So Many Applications Go Sideways

Most of the trouble doesn't come from the loan itself. It comes from walking in unprepared.

Here's what usually goes wrong:

- People apply before checking their own credit report, so they get surprised by a denial they didn't see coming.

- They guess at how much to borrow, asking for either too little or too much.

- They skip reading the loan terms, then get blindsided by fees buried in the fine print.

- They apply to several lenders at once out of panic, which can quietly lower their credit score.

- They submit incomplete paperwork, which stalls the process for days or even weeks.

None of these mistakes happen because someone is careless. They happen because nobody hands you a clear checklist before you start.

The Hidden Cost of Getting This Wrong

A messy loan application doesn't just waste your time. It chips away at something harder to measure.

- You start dreading your inbox, afraid of seeing another rejection email.

- You feel embarrassed asking a loan officer questions that feel "too basic."

- You begin doubting your own financial judgment, even when the system is what's confusing.

- You put off applying altogether, even when you genuinely need the money.

- Stress from money problems can affect your sleep, focus, and even your relationships.

- You start comparing yourself to friends or coworkers who seem to "have it figured out," even though most of them struggled through the same confusion at some point too.

None of this means something is wrong with you. It means the process needs a clearer map, which is exactly what the rest of this guide is built to give you.

Take Daniel, a delivery driver in Texas. His car broke down and he needed $4,000 fast. He applied to four lenders in a single afternoon, hoping one would approve him quickly.

Two rejected him outright. One approved him but buried a steep origination fee in the contract he almost missed. By the time he found the right lender, three days had passed and his car sat in the shop the entire time.

Daniel's story isn't rare. It happens because loan websites are built to get clicks, not to walk you through the process step by step.

That's exactly what we're going to fix together. A personal loan application doesn't have to feel like a maze. Once you know the order of operations, the entire process becomes almost mechanical, the kind of thing you can knock out in one sitting instead of one stressful week.

Your Step-by-Step Checklist for Applying With Confidence

Let's turn this into something simple. Three steps now, two more coming in the next part of this guide.

Step One: Know Your Numbers Before You Touch a Single Application

Before you fill out anything, pull your credit report and figure out your real score.

You can get a free copy from each major credit bureau once a year through the official government-authorized site. Many bank apps also show a free, regularly updated score.

While you're checking, it's worth scanning for anything that looks off. Disputing errors on your credit report before you apply can raise your score by a noticeable amount within a few weeks.

While you're at it, calculate two more numbers:

- Your debt-to-income ratio. Add up your monthly debt payments and divide by your gross monthly income. Most lenders prefer this under 40%.

- Your monthly budget ceiling. Figure out exactly how much you can comfortably pay each month before you even start browsing loan amounts. Tracking your daily spending for a couple of weeks makes this number much easier to pin down accurately.

Think of this step like checking your gas tank before a road trip. Skipping it doesn't make the trip shorter, it just makes a breakdown more likely halfway through.

Step Two: Decide Exactly How Much You Need, Not How Much You Want

This step trips up more people than you'd think. Borrowing too little means you'll need a second loan later. Borrowing too much means paying interest on money you didn't actually need.

Write down the exact purpose of your loan and the exact dollar amount tied to it.

A few real-life scenarios to picture, so this feels less abstract:

- If you're consolidating $7,500 in credit card debt, borrow $7,500, not a rounded-up $10,000 "just in case."

- If a $3,200 medical bill is the reason, request that number, plus a small buffer for any related costs you can clearly justify.

- If you're covering a planned expense like a move, get an actual quote first instead of guessing.

Lenders also respond better to specific, well-explained loan purposes. A clear reason on your application can make the underwriting process faster, since it removes guesswork on their end too.

This single habit, writing down a real number tied to a real reason, often separates a smooth approval from weeks of back-and-forth questions from the lender.

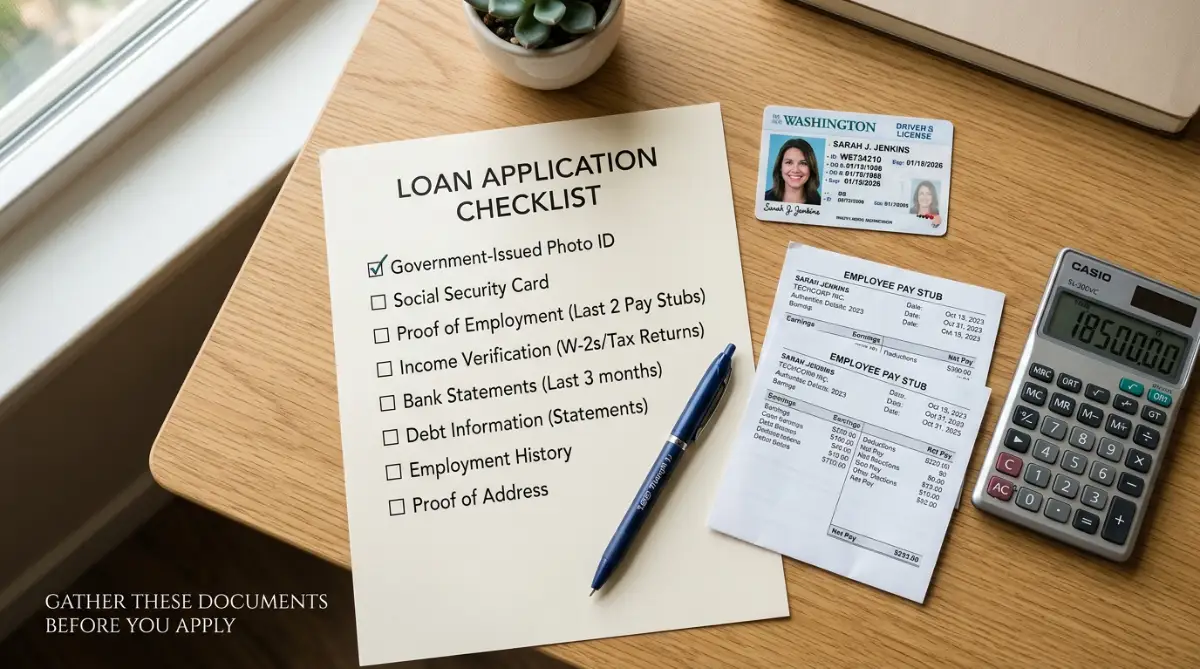

Step Three: Gather Every Document Before You Start the Application

This is the step most people skip, and it's the one that causes the most delays.

Having your paperwork ready before you apply can cut your approval time from days down to hours.

Here's a simple list to pull together in advance:

- Government-issued photo ID, such as a driver's license or passport.

- Proof of income, like recent pay stubs, tax returns, or bank statements if you're self-employed.

- Proof of address, such as a utility bill or lease agreement.

- Social Security number or taxpayer ID, required for identity verification.

- A list of your current debts, including balances and minimum monthly payments.

Picture this step like packing for a flight the night before instead of the morning of. Everything in one place means no last-minute scrambling.

Check Prequalification Before You Submit a Full Application

Here's a detail that saves people a lot of stress. Most lenders let you check your likely rate through a soft credit pull, which does not affect your score at all.

This is different from the full application, which triggers a hard credit pull once you formally apply. Use the soft-pull option first, every time it's available. The difference between hard and soft credit pulls is worth understanding fully before you submit anything formal.

A simple way to think about it: prequalification is like trying on shoes in the store. Applying is like actually buying them. You want to know they fit before you commit.

Here's how this plays out in practice. Maria, a teacher in Arizona, wanted a $6,000 loan to cover a home repair. Instead of applying blind, she used prequalification tools on four different lender websites first.

Two of them showed rates she didn't love. One showed a rate she was happy with. She moved forward with a single formal application instead of four, protecting her score the entire time.

Why Doing These Three Things First Changes Everything

Each one of these steps builds directly on the last. Knowing your numbers tells you which lenders will even consider you. Knowing your exact loan amount keeps you from over-borrowing or under-borrowing. Having your documents ready turns a multi-day process into something you can often finish in one sitting.

This isn't about being perfect. It's about removing the guesswork that causes most applications to stall out or get denied.

Clearing Up a Few Things Borrowers Often Get Wrong

A handful of beliefs trip people up before they even start their application. Let's clear them up.

"Prequalifying guarantees approval." It doesn't. Prequalification gives you an estimate based on a soft credit check, but the lender still verifies everything during the full application.

"Applying online is less safe than applying in person." Reputable online lenders use the same encryption standards as banks. The bigger risk is applying through an unfamiliar site that lacks clear contact information or physical verification, not the format itself.

"A cosigner is required if my income is low." A cosigner is optional in almost every case. It simply gives you a stronger application if your income or credit history is thin on its own.

"All lenders check the same things." Some weigh credit score heavily. Others weigh income or banking history more. This is exactly why comparing more than one lender matters, even when your numbers feel borderline.

"Once I submit, I can't change the loan amount." Many lenders allow adjustments before final funding, especially if you realize you requested slightly more or less than you actually need.

Borrowers who prepare this way consistently report smoother approvals and fewer surprises once they reach the offer stage. The difference between a frustrating application and a fast one almost always comes down to what happens before you click "Submit," not after.

In the next part of this guide, we'll walk through how to actually compare lenders side by side, what to expect during the approval and funding stages, and the final checks worth doing before you accept any loan offer.

Think back to Daniel from earlier. If he had spent twenty minutes pulling his credit report and gathering his pay stubs before applying anywhere, he likely would have avoided two of those four rejections completely. The lenders that turned him down weren't being unreasonable, they simply needed information he hadn't prepared yet.

That's the real shift this checklist creates. You stop reacting to whatever a lender's website throws at you, and you start walking in with everything already lined up. The process feels less like a test you might fail and more like a form you're simply filling out correctly the first time

Comparing Offers the Smart Way Once You're Approved

Getting one approval feels like a win. But the real win happens when you compare it against at least one or two others before signing anything.

This step separates borrowers who get a fair deal from borrowers who quietly overpay for years without ever realizing it.

Look at the APR, Not Just the Interest Rate

A lot of people stop at the interest rate and call it done. That number alone doesn't tell the whole story.

The APR, or annual percentage rate, bundles in the interest rate plus most fees, giving you a single number that reflects the true cost of borrowing. Two loans can show the same interest rate and still cost very differently once you compare their APRs.

Here's a simple way to picture it. Imagine two coffee shops selling a "cup of coffee" for the same listed price. One charges an extra fee for the cup itself, the other doesn't.

The sticker price looked identical, but your total bill wasn't. Loan rates work the same way, which is exactly why the APR matters more than the headline number.

A loan advertised at 11% interest with a 5% origination fee can easily carry a higher APR than a competing loan at 12.5% interest with no fee at all. Always ask each lender for the APR directly if it isn't shown clearly on their offer page.

Understand Whether Your Rate Is Fixed or Variable

Most personal loans come with a fixed rate, meaning your payment stays the same for the entire term. Some lenders offer variable rates instead, which can rise or fall with broader market conditions.

For most borrowers building stability, a fixed rate is the safer, more predictable choice. You know exactly what you owe every month, with no surprises six months down the road.

If a lender offers a variable rate at a noticeably lower starting number, ask directly how high it could climb and how often it adjusts. A "low" rate today isn't helpful if it can jump unexpectedly next year.

Ask About Discounts You Might Already Qualify For

A lot of lenders offer small rate discounts that never show up on the homepage. You usually have to ask.

Common examples include a discount for setting up autopay, a loyalty discount if you already bank with that institution, or a slightly better rate for choosing a shorter repayment term. None of these are guaranteed, but asking costs nothing.

A quick phone call or chat message asking "Do you offer any rate discounts I might qualify for?" takes under five minutes. Skipping that question is a missed opportunity that costs real money over the life of the loan, sometimes adding up to more than you'd expect from one short conversation.

Know What Happens Between Submitting and Getting Funded

A few predictable steps usually follow once you accept an offer. Knowing them ahead of time keeps you from panicking over a normal part of the process.

- Identity verification. Some lenders call or email to confirm details on your application match your documents.

- Final document requests. Don't be surprised if they ask for one more pay stub or a clearer photo of your ID.

- E-signing the agreement. Read every page before you sign, even if it feels long. This is your actual contract.

- Funding timeline. Many online lenders deposit funds within one to two business days after final approval, though some same-day options exist.

Think of this stage like the final walkthrough before buying a house. You've already agreed on the big picture, but this is your last chance to catch anything before it's final.

A borrower named Priya, a graphic designer in Florida, almost skipped reading her final agreement because she was excited to get funded quickly. A friend convinced her to spend ten extra minutes reading it first.

That ten minutes revealed a prepayment penalty she hadn't expected, buried on page three. She called the lender, confirmed the term, and decided it still worked for her plan, but she made that choice with full information instead of finding out the hard way later.

Keeping Your Finances Steady After the Loan Lands

Getting funded isn't the finish line. What you do in the first few months after funding matters just as much as the application itself.

A few habits keep things running smoothly once the money is in your account:

- Set up autopay immediately, so your very first payment never slips through the cracks.

- Mark your due date on a calendar, even with autopay active, as a backup reminder.

- Build a simple repayment budget, treating your new loan payment like any other fixed monthly bill.

- Avoid opening new credit accounts right away. Wait at least a few months so your credit profile has time to settle.

- Set aside a small buffer for unexpected costs, so a single surprise expense doesn't force you to miss a payment. Even a small emergency fund built up over a few months can protect the progress you just made.

Borrowers who treat the first ninety days after funding with this kind of attention tend to avoid the most common slip-ups entirely. The loan becomes just another predictable line item instead of a source of stress.

The Slip-Ups That Trip Up Even Careful Applicants

A handful of mistakes show up again and again during the application process. Spotting them ahead of time means you can sidestep every one.

Mistake One: Signing Before Reading the Full Agreement

It's tempting to scroll straight to the signature box when you're excited about getting funded. Resist that urge completely.

Loan agreements often include details on late fees, prepayment penalties, and default terms that never show up in the marketing email. Reading the full document takes ten minutes and can save you from an unpleasant surprise later.

For example, a late fee clause might charge $35 or 5% of your payment, whichever is higher. On a $400 monthly payment, that's a $20 surprise you'd rather know about in advance than discover after a missed due date.

Mistake Two: Giving Inconsistent Information Across Documents

If your pay stub lists one address and your ID lists another without explanation, it can stall your approval or trigger extra verification steps.

Double-check that your name, address, and income details match across every document before you submit anything. Small inconsistencies cause disproportionately large delays.

Mistake Three: Borrowing Without a Clear Repayment Plan

Getting approved feels good, but approval isn't the same as a plan. Some borrowers accept funding without mapping out exactly how the new payment fits their monthly budget.

This is where pairing your loan with a structured repayment approach, like the debt snowball method, can keep you organized if this loan is part of a larger debt payoff plan rather than a single isolated expense.

Picture two borrowers who both get approved for $8,000 consolidation loans. One writes out exactly which accounts the funds will close and tracks the payoff order. The other deposits the money and lets it blend into a general checking balance.

Six months later, the first borrower has a clean, predictable single payment. The second still has three nearly-maxed cards, because the loan money quietly covered everyday spending instead of the debt it was meant for.

Mistake Four: Ignoring the Prepayment Penalty Question

Not every loan charges a fee for paying it off early, but plenty do. Skipping this question can cost you if your financial situation improves and you want to pay the loan off ahead of schedule.

Always ask directly: "Is there any penalty for paying this loan off early?" A simple yes or no answer here can change your entire payoff strategy.

Mistake Five: Letting the Offer Expire Before Acting

Most loan offers come with a deadline, often somewhere between 7 and 30 days. Letting that window close means starting the entire process over, sometimes with a fresh hard inquiry.

Treat your accepted offer like a flight booking with a check-in deadline. Once you decide to move forward, finish the remaining steps within a few days rather than letting the offer sit untouched.

What These Mistakes Actually Cost You

None of these slip-ups are dramatic on their own. Together, they add up to real money and real stress, often in ways that don't show up until weeks or months later.

A missed prepayment penalty question can cost hundreds of dollars if you try to pay off the loan early. An expired offer means redoing paperwork and potentially facing a new hard inquiry on your credit report.

The good news is that every single mistake on this list is completely avoidable. None of them require special financial training, just a few extra minutes of attention at the right moments in the process.

You Already Know More Than Most First-Time Applicants

A personal loan application doesn't have to feel like a guessing game anymore. You now know how to check your numbers, gather your documents, compare offers properly, and avoid the mistakes that trip up so many other borrowers.

That puts you in a stronger position than most people who walk into this process completely blind.

Pick one thing from this guide and act on it today. Maybe it's pulling your credit report this afternoon. Maybe it's writing down the exact dollar amount and reason for the loan you need.

Small, deliberate steps like these turn a stressful process into a simple checklist you control from start to finish. You're not just applying for a loan anymore, you're applying with a plan, and that difference shows up in every part of the process from approval to your very first payment.

Think back to Daniel and Priya from earlier in this guide. Neither of them needed a finance background to get this right. They just needed a clear order of steps to follow, the same steps you're walking away with right now.

The next time someone you know mentions feeling stuck or overwhelmed applying for a loan, you'll likely find yourself explaining exactly what to check first. That's usually a good sign you've actually learned something worth holding onto.