Why Picking Between State Farm and Geico Feels So Confusing

You open your laptop to compare car insurance quotes. Ten minutes later, you have twelve browser tabs open and zero answers.

This is the reality for most people shopping for auto insurance. You just want a fair price and real protection. Instead, you get confusing terms, mixed reviews, and pressure to decide fast.

State Farm and Geico are two of the biggest names in the industry. Both promise savings. Both promise great service. Groups like the Insurance Information Institute recommend comparing at least three insurers before you decide, so weighing these two carefully is already a smart start. So how do you actually choose?

Why People Struggle to Find the Right Answer

Most drivers do not fail because they are careless. They fail because the information out there is scattered and often outdated. Even the NAIC's official consumer guide to auto insurance can feel dense if you do not already know what you are looking for.

Here is what usually goes wrong:

- People compare price alone and ignore coverage gaps

- Online reviews are mixed, so it is hard to know who to trust

- Insurance jargon like "liability limits" or "comprehensive deductible" is never explained simply

- Friends and family give advice based on their own state, driving history, or car type, which may not apply to you

- Comparison sites often push whichever company pays them the most, not whichever fits your needs

How This Confusion Affects You

This is not just a paperwork problem. It quietly affects your peace of mind.

- You worry you are overpaying every single month

- You feel unsure if you would actually be covered after a real accident

- You second-guess your choice every time you see a car insurance ad

- You avoid switching companies because the process feels overwhelming

- You lose confidence in your own ability to make a smart financial decision

That last point matters more than people admit. Car insurance is not just a bill. It is a decision that touches your safety, your savings, and your sense of control over your own life. As Consumer Reports explains in its car insurance buying guide, your premium depends on far more than your driving record alone, which is part of why the process feels so overwhelming.

The good news is that this decision does not have to stay confusing. Once you understand what actually separates State Farm from Geico, the choice becomes a lot clearer. Let's break it down step by step.

A Simple Way to Compare State Farm and Geico

You do not need to be an insurance expert to make a smart choice here. You just need a clear process.

Below is a simple, three-step approach that works whether you are buying your first policy or switching after years with the same company.

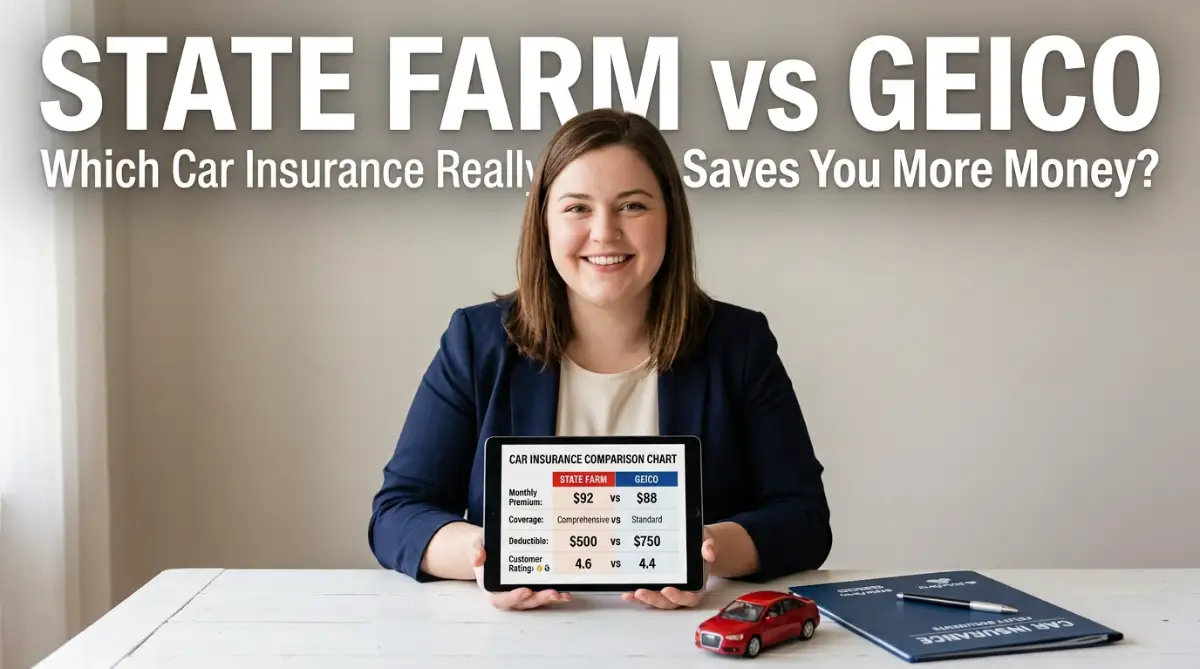

Step 1: Look at Real Quotes, Not Assumptions

The biggest mistake people make is assuming one company is "always cheaper." That is rarely true.

Geico is often known for competitive online pricing, especially for drivers with a clean record who prefer managing everything through an app. State Farm tends to shine for drivers who want a local agent and are open to bundling home and auto insurance for extra discounts.

Think of it like grocery shopping. One store might have cheaper produce, but the other has better deals on meat and dairy. You will not know which is better for your basket until you actually check both.

Here is a quick way to test this yourself:

- Request a quote from both companies using the exact same coverage limits

- Include the same deductible amount on each quote

- Ask about every discount you qualify for, such as safe driver, good student, or multi-policy discounts

- Compare the final price, not just the advertised "starting" rate

Doing this takes maybe twenty minutes. But it removes all the guesswork and replaces it with real numbers based on your situation.

Step 2: Match Coverage to How You Actually Drive

Price only tells half the story. The real question is whether the policy protects you the way your life actually needs.

Ask yourself these questions before comparing anything else:

- Do you drive long distances daily, or mostly short local trips?

- Is your car brand new, financed, or older and paid off?

- Do you live in an area with heavy traffic, harsh weather, or high theft rates?

- Do you want extras like roadside assistance or rental car coverage?

If you drive an older car with no loan, you might not need full comprehensive coverage, which could lower your premium with either company. If your car is financed, your lender will likely require higher coverage limits, and both State Farm and Geico can meet that requirement, just with different pricing structures.

Geico's coverage options are usually straightforward and easy to customize online. State Farm often gives you more flexibility to talk through your specific situation with a local agent, which can help if your needs are a bit unusual, like owning multiple vehicles or a teen driver on your policy.

Neither approach is automatically better. It depends on whether you prefer a hands-on digital experience or a face-to-face conversation with someone who knows your file.

Step 3: Check the Claims Experience Before You Need It

This step gets skipped by almost everyone, and it is the one that matters most.

You do not really find out how good an insurance company is until you file a claim. By then, it is too late to switch if you are unhappy.

So test it in advance:

- Search for recent customer reviews specifically about the claims process, not just pricing

- Call customer service with a question and note how fast and helpful the response is

- Ask if claims can be filed and tracked through a mobile app

- Ask about average repair time and rental car coverage during claims

Geico has invested heavily in a fast, app-based claims process, which many customers describe as simple and quick for straightforward accidents. State Farm's large agent network can offer a more personal touch, especially for complicated claims involving multiple parties or significant damage.

Think of your insurance company like a spare tire in your trunk. You barely think about it most of the time. But when you actually need it, you want it to work without a fight.

Putting It All Together

Once you have real quotes, coverage that matches your driving life, and a sense of how each company handles claims, the decision usually becomes obvious. There is no single "winner" that fits everyone.

If you value a simple app, competitive online pricing, and fast digital claims, Geico is often a strong fit. If you prefer a local agent, easy bundling with home insurance, and a more personal claims experience, State Farm tends to be the better choice.

The smartest move is not picking the "best" company on paper. It is picking the one that matches how you actually want to manage your insurance day to day.

You do not have to get this decision perfect on the first try either. Insurance policies are not permanent. You can request new quotes every year, especially after big life changes like moving, buying a new car, or improving your driving record. Staying flexible protects both your wallet and your peace of mind over time.

Take twenty minutes this week, pull quotes from both companies, and compare them side by side using the steps above. That small effort now can save you real money and real stress later.

Two Pro-Level Moves That Save Long-Time Drivers Even More

Getting a good quote once is a great start. Keeping that good rate for years is a different skill.

Most people set up their policy and never touch it again. That is exactly how you end up quietly overpaying without noticing.

Here are two moves that experienced drivers use to squeeze out extra savings, no matter which company they pick.

Stack Every Discount You Actually Qualify For

Both State Farm and Geico offer a long list of discounts. Most drivers only claim two or three of them.

Think about it like a loyalty punch card at a coffee shop. If you never ask the barista to stamp it, you never get the free drink, even though you paid for every cup along the way.

Here are discounts people often forget to ask about:

- Paying your full premium up front instead of monthly

- Setting up paperless billing and automatic payments

- Completing a defensive driving or safe driving course

- Insuring more than one car on the same policy

- Keeping a clean claims history for several years in a row

Geico tends to list its discounts clearly inside its app or website, so you can check them off yourself. State Farm's local agents can often manually apply discounts you did not know you qualified for, especially if you ask directly during a policy review call.

Either way, the discount will not apply itself. You have to ask.

Let a Usage-Based Program Work in Your Favor

If you are a careful driver, a usage-based or telematics program can lower your rate in a way flat pricing never will.

These programs use a mobile app or small device to track things like:

- How hard you brake

- How fast you accelerate

- What time of day you usually drive

- How many miles you drive each month

Both State Farm and Geico offer their own version of this kind of program. If you already drive gently and avoid late-night trips, this is close to free money sitting on the table.

Picture two neighbors with identical cars and identical coverage. One drives calmly and hits the brakes early. The other tends to speed up to yellow lights. Over a year, a telematics program can create a real price gap between those two drivers, even though their policies started out the same.

Bundle Policies Without Overpaying for Coverage You Do Not Need

Bundling your car insurance with renters or homeowners insurance is one of the most talked-about ways to save. It genuinely works, but only if you check the total price, not just the discount percentage.

Here is the trap people fall into. A company advertises "save up to 25 percent" on bundled policies. That sounds great, but 25 percent off a higher starting price can still cost more than a separate policy from a different company at a lower base rate.

Treat a bundle offer like a restaurant combo meal. A combo can be a great deal, or it can just be a way to sell you a bigger drink you did not need. The only way to know is to compare the final total, item by item, against buying things separately.

Both State Farm and Geico offer bundling options, but the size of the discount and the base pricing behind it can differ a lot depending on your state and your home insurance provider. Always ask for the bundled price and the separate prices side by side before you commit.

Making the Good Rate Last

A good quote today does not guarantee a good rate three years from now. Insurers adjust pricing based on claims trends, your driving record, and even where you park overnight.

Set a yearly reminder to re-check your rate, the same way you would recheck your phone bill or streaming subscriptions. This single habit, done once a year, is one of the easiest ways to make sure you are not slowly overpaying.

Think about a driver named Sarah who signed up for a great rate five years ago and never looked at it again. By year five, her neighbor with a nearly identical car and driving record was paying almost 20 percent less, simply because he requested a new quote every renewal period. Sarah was not doing anything wrong. She was just not checking.

If insurance is one of several bills quietly eating into your paycheck, it also helps to zoom out and look at building a real monthly budget so every dollar, including your premium, has a clear job.

Mistakes That Quietly Cost Drivers Hundreds of Dollars

Even smart, careful people make these mistakes when picking between State Farm and Geico. The good news is that every single one is avoidable.

Mistake 1: Choosing Based on Price Alone

The cheapest policy is not always the best deal. A low premium can hide low coverage limits that leave you paying out of pocket after a real accident.

Always compare the coverage limits side by side, not just the monthly cost. A $30 difference in premium means very little if one policy covers half as much damage.

Imagine two drivers get into similar accidents. One has a policy with low liability limits chosen purely for the cheap price, and ends up personally owing thousands of dollars after the payout runs out. The other paid slightly more each month but never had to touch personal savings. The second driver made the smarter long-term choice, even though their receipt looked worse on paper.

Mistake 2: Letting Your Policy Auto-Renew Without Checking

Most insurers automatically renew your policy every six or twelve months. This is convenient for them, not always for you.

Rates quietly creep up over time, especially if you never call to ask about new discounts. A policy that was competitive two years ago may not be competitive today.

Mistake 3: Giving Inaccurate Information to Save Money

Some drivers underreport their mileage or leave a household driver off the policy to lower the price. This can seriously backfire.

If you ever file a claim and the insurer discovers the information was wrong, your claim can be reduced or denied entirely. The short-term saving is not worth the long-term risk.

A common example is leaving a teenage driver off the policy to keep the price down, then having that same teen involved in an accident while borrowing the car. Because the driver was not listed, the claim can be investigated far more closely, delayed, or denied outright, turning a small monthly saving into a massive unexpected bill.

Mistake 4: Dropping Coverage You Actually Need

Cutting comprehensive or collision coverage on a financed car can violate your loan agreement. It can also leave you owing money on a car you can no longer drive.

Before removing any coverage, check your loan or lease terms first, not just your budget. A quick call to your lender can save you from a costly surprise later.

Consider a driver who drops comprehensive coverage on a financed car to save fifteen dollars a month, then has the car stolen from a parking lot. Without comprehensive coverage, there is often no payout for theft, yet the driver still owes the full remaining loan balance to the lender. The small monthly saving turns into a debt with no vehicle to show for it.

Mistake 5: Ignoring the Fine Print on Extras

Roadside assistance, rental car coverage, and gap insurance all sound similar but work very differently between companies. Skipping the fine print here is one of the most common regrets people share after an accident.

Ask directly what is and is not included in any add-on before you assume you are covered. A five-minute question can prevent a very expensive misunderstanding.

Avoiding these five mistakes protects more than your premium. It protects the payout you actually count on when something goes wrong. None of these mistakes require bad luck to become expensive. They only require a little bit of inattention, which is exactly why they catch so many careful, well-meaning drivers off guard. If unexpected costs are a repeat stress point for you, it may also help to start tracking your daily spending so surprise expenses like a rate increase do not catch you off guard.

You Are More Capable of This Decision Than You Think

Here is the honest truth. There is no universal "best" between State Farm and Geico. There is only the best fit for your car, your driving habits, and your budget.

You now know how to get real quotes instead of guessing. You know how to match coverage to your actual life instead of copying a stranger's policy. You know how to check the claims experience before you ever need it, and you know the discounts and mistakes that separate confident shoppers from confused ones.

That is more than most drivers ever learn.

Most people never revisit their car insurance until something forces them to, like a rate hike letter or a stressful accident. You are already ahead simply by taking the time to understand how this decision actually works. That puts you in a small group of drivers who make this choice on purpose instead of by default.

If your credit history is part of what is driving your premium up, working on improving your credit score can help lower your rate over time in many states. And once you start saving money from better coverage and smarter discounts, moving those savings into a high-yield savings account instead of letting it sit idle in a regular checking account puts that extra money to work for you.

You do not need to have this perfectly figured out today. You just need to take the first small step.

Pull one quote. Ask one question you have been putting off. Compare one thing you have never compared before. That single action moves you from confused to in control, and it is the same first step that leads every confident driver to the policy that finally fits.

There is no perfect time to do this. Your current policy will keep renewing on its own whether you check it or not, quietly locking in whatever rate it has, good or bad. The drivers who end up paying less over the years are rarely the ones with the most complicated strategy. They are simply the ones who ask the right questions a little more often than everyone else. You now have those questions. Use them.

Disclaimer:

This article is written for general informational purposes only and does not constitute financial, legal, or insurance advice. Insurance rates, coverage options, and discounts vary based on your location, driving history, vehicle, and individual circumstances. Please contact State Farm, Geico, or a licensed insurance agent directly to get accurate, personalized quotes before making any decision.